Falling Costs Drive Strong Demand for Australia’s Residential Solar PV

Newsletter

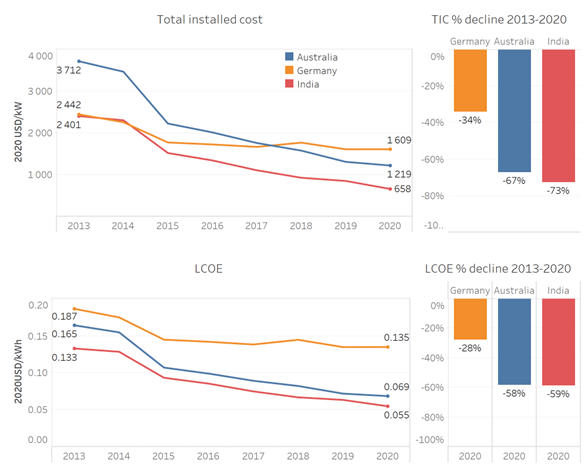

Australian residential solar photovoltaic (PV) systems now have some of the lowest costs in the world, encouraging households to invest in rooftop solar PV at a time of rising energy prices. In 2010 total installed costs in Australia were about 50 percent higher than in Germany, but after continuous cost declines, in 2020 Australian systems were found to cost around a quarter less than in Germany. The Australian market’s long-established suppliers, experienced installers and consistent demand have all helped see costs continue to decline.

The cost of residential rooftop PV electricity (known as the levelised cost of electricity, or LCOE) in Australia declined steeply in the period 2010-2020, falling to USD 0.069 per kilowatt hour (kWh). This represents a drop of 58 per cent in the Australian residential LCOE. IRENA’s data also shows that between 2013 and 2020 total installed costs (prior to subsidy) fell by 67 per cent in 2020 US dollar terms for residential systems in Australia.

Total installed costs, LCOE and cost reductions for residential PV in Australia, Germany and India, 2013-2020.

Note: TIC = total installed cost.

Sources: IRENA Renewable Cost Database and Solar Choice.

The benefits of falling prices for residential solar PV are not just being felt in Australia: since 2010 a declining trend in installed costs has been visible in a wide range of markets. Cost reductions have changed the competitiveness of rooftop solar PV in both the residential and commercial sectors in the past decade. The LCOE of residential PV systems in Australia, Germany, Italy, Japan and the United States declined from around 30¢-46¢ per kWh in 2010 to just 5¢-24¢ per kWh in 2020. This remarkable decline has been driven primarily by declines in PV module prices, which have fallen by 93 per cent on a wholesale basis since 2010, as module efficiency has improved, and manufacturing has increasingly scaled up and been optimised.

Domestic electricity storage is also taking off in Australia. The improved competitiveness of solar PV, the country’s excellent solar resources, falling battery costs, and high and often rising residential electricity prices in Australia have led to increased use of solar PV systems with electricity storage to reduce electricity costs to households.

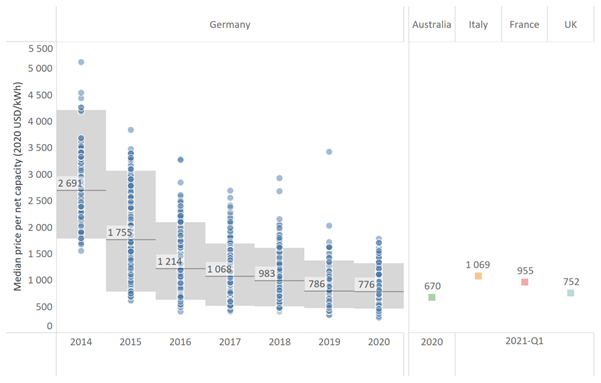

The downward trend in battery prices in particular should not be overlooked, as it has contributed to the improved economics of such systems. In Germany, for example, between 2014 and 2020 the price of behind-the-meter residential lithium-ion battery systems fell by 71 per cent, to USD 776 per kWh of usable capacity. Data for Australia suggest prices were somewhat lower than those experienced in Germany for small-scale residential battery storage systems, while the United Kingdom also experiences slightly lower prices. Battery storage systems in Italy and France are somewhat more expensive, which mirrors the higher rooftop solar PV pricing in these countries.

Behind-the-meter residential lithium-ion battery system prices in selected countries, 2014-2021-Q1.

These developments have had an improving effect on the economics of residential systems that combine solar PV with electricity storage. Despite the additional upfront investment that batteries call for, overall savings can still be realised from the residential consumer perspective after the payback period. Adding electricity storage to the PV system allows higher self-consumption rates to be achieved, reducing the impacts of increasing electricity prices. And since feed-in tariff levels have declined below the prevalent electricity price, offsetting the risk of increasing electricity prices with self-consumption has been an important driver for the increased adoption of such systems.

Data from the IRENA Renewable Cost Database confirms the remarkable improvement in the competitiveness of solar PV between 2010 and 2020, and not only in the residential sector. During the decade, the installed cost of utility-scale solar PV declined by 81 per cent on a global average basis, to USD 883 per kW. This means that the cost fell by a third every time the cumulative installed capacity doubled. Generally, the utility sector has lower costs than the residential rooftop solar PV market due to the larger scale of its systems. Accordingly, the global weighted‑average LCOE of utility‑scale solar PV fell by 85 per cent during that period, from 38¢ per kWh to just 6¢ per kWh. This has allowed utility-scale solar PV increasingly to undercut even the cheapest options among new fossil-fuelled power plants.

Since 2013, data for more markets beyond the early-adopter countries has also become available. The importance of accurate cost estimates has persisted as PV markets have grown and evolved, to understand the drivers of cost reduction and market growth.

As the data demonstrates, the dramatic declines in the cost of rooftop solar PV are continuing to drive up demand for these systems in Australia and similar markets, allowing households to moderate energy price rises with self-consumption. There is every reason to believe that the improving economics of rooftop solar PV can bring welcome cost savings to households in dozens more countries across the world.

The IRENA Renewable Costing Alliance is part of the Agency’s continuous work to gather precise, reliable information and data on the rapidly improving cost profile of renewable energy sources and technologies. As an early member of the IRENA Renewable Costing Alliance, Solar Choice has been sharing its survey data with IRENA since 2015.

Expert Insight by:

Michael Taylor

Senior Analyst, Renewable Energy Cost Status and Outlook, IRENA

© IRENA 2025

Unless otherwise stated, material in this article may be freely used, shared, copied, reproduced, printed and/or stored, provided that appropriate acknowledgement is given of the author(s) as the source and IRENA as copyright holder.

The findings, interpretations and conclusions expressed herein are those of the author(s) and do not necessarily reflect the opinions of IRENA or all its Members. IRENA does not assume responsibility for the content of this work or guarantee the accuracy of the data included herein. Neither IRENA nor any of its officials, agents, data or other third-party content providers provide a warranty of any kind, either expressed or implied, and they accept no responsibility or liability for any consequence of use of the content or material herein. The mention of specific companies, projects or products does not imply that they are endorsed or recommended, either by IRENA or the author(s). The designations employed and the presentation of material herein do not imply the expression of any opinion on the part of IRENA or the author(s) concerning the legal status of any region, country, territory, city or area or of its authorities, or concerning the delimitation of frontiers or boundaries.