Status and pace of progress

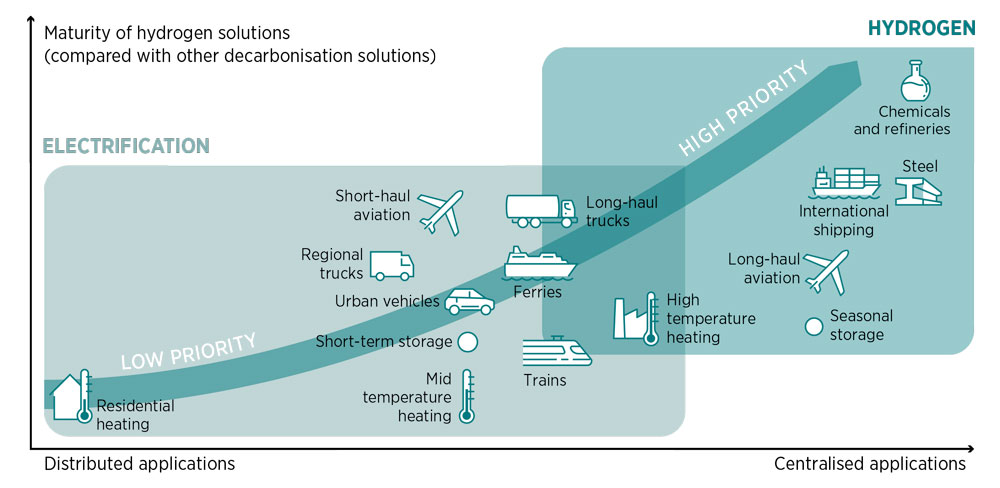

Direct electrification is difficult, if not impossible, in some end-use sectors, including steel-making, chemical production, long-haul aviation and maritime shipping. But there is a viable solution for decarbonising these end uses – “green” hydrogen and other fuels produced from renewable electricity (Figure 7.1) (IRENA, 2022e). IRENA’s 1.5°C Scenario projects that by 2050, clean – green and blue – hydrogen production will grow to 523 million tonnes per year by 2050 (IRENA, 2023). Hydrogen can also serve as an excellent energy storage medium.

However, green hydrogen adoption remains low compared with required deployment levels, due to relatively high costs. In Europe, green hydrogen’s average levelised cost is between USD 4.5/kg and USD 6/kg. In the United States, the 2022 Inflation Reduction Act offers a USD 3/kg subsidy, which could bring the levelised cost of hydrogen down below USD 2/kg, making green hydrogen competitive.

FIGURE 7.1 | End-use applications where clean hydrogen can be an effective alternative for deep decarbonisation: Clean hydrogen policy priorities

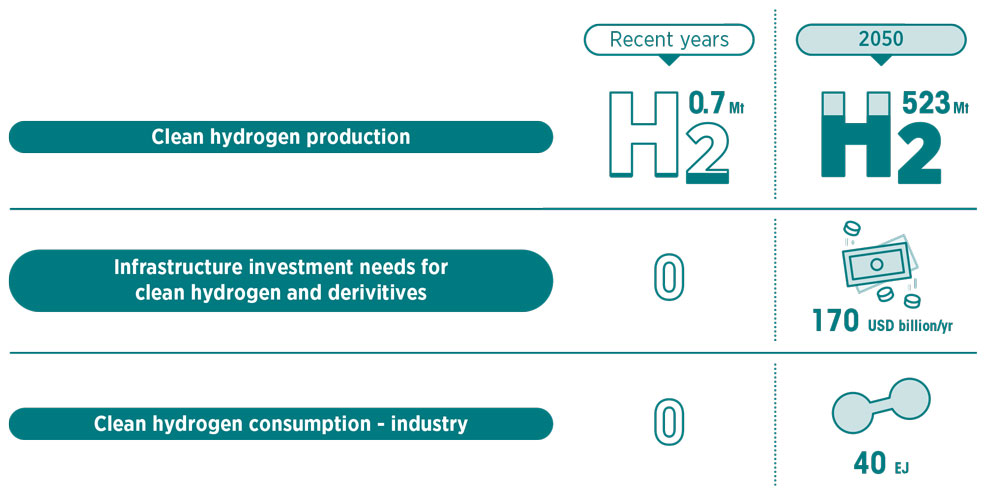

In IRENA’s 1.5°C Scenario (Figure 7.2), the production of green hydrogen and its derivatives must increase from today’s negligible levels to 125 million tonnes of hydrogen (MtH2)/year by 2030 and 523 MtH2/year by 2050 (94% of global hydrogen production). Such a significant increase in production will require substantial investments in electrolysers and other technologies to produce, deliver and use green hydrogen fuels; IRENA’s 1.5°C Scenario calls for investments of USD 170 billion/year through 2050.

FIGURE 7.2 Green hydrogen production, investment and consumption in IRENA’s 1.5°C Scenario

Notes: 316.67 Mt = 38 EJ. EJ = exajoule; Mt = million tonnes.

In IRENA’s 1.5°C Scenario, by 2050, the industrial sector would use 40 EJ from clean hydrogen per year, particularly in chemicals, and iron and steel, while the transport sector would require 21 EJ from hydrogen and its derivatives (IRENA, 2023). Some of the hydrogen would be converted into chemical derivatives – such as ammonia, methane and methanol – and synthetic fuels, which are known as “Power-to-X” products. These hydrogen-based products can be directly used as transport fuels or chemical feedstocks, or for seasonal energy storage. Green hydrogen also supports the integration of renewables, offers long-term energy storage and can accelerate the growth of clean industries, such as steel in India, ammonia and fertilisers in Egypt and Trinidad and Tobago, or cement in Viet Nam and Indonesia (Cordonnier and Saygin, 2022).

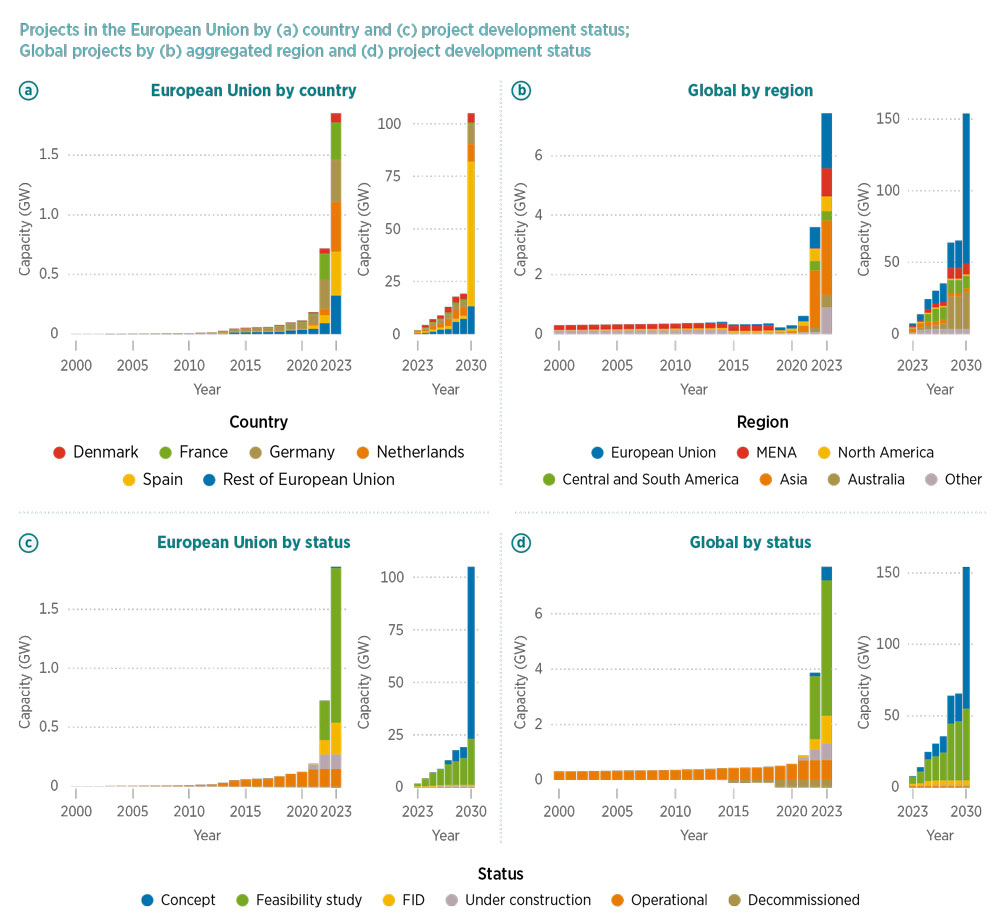

To produce enough green hydrogen and derivatives to meet the climate goals outlined in the Paris Agreement, global electrolyser capacity must grow 6 000 to 8 000 fold from today’s negligible 0.5 MW up to 350 GW in 2030 and roughly 5 000 GW in 2050 (Figure 7.3). However, while the number of recent project announcements suggests that capacities will increase exponentially in the coming years, final investment decisions have not yet been made for 80% of the announced capacity (Odenweller et al., 2022). Nevertheless, more than 60 countries have developed, or are in the process of developing, national hydrogen strategies, and many emerging and developing countries have abundant low-cost renewable energy resources, which paves the way for competitive hydrogen markets (IRENA, 2022e). Using these resources to produce green hydrogen would enable these countries to reap major social and economic benefits, such as reduced dependence on imported fossil fuels, increased access to clean energy and creation of new export markets.

FIGURE 7.3 Historical development and future announcements of electrolysis projects

Notes: Each panel is divided into two parts. The main, left-hand part shows 2000-2023 data, while the smaller right-hand part with a separate axis shows 2023-2030 data. Projects without a specified starting date (accounting for 21 GW in the European Union and 127 GW globally) are omitted in all the panels. Panels a and b have figures corresponding to decommissioned projects omitted. FID = final investment decision; GW = gigawatt; MENA = Middle East and North Africa.

7.1 Importance of smart electrification in the development of green hydrogen

The use of green hydrogen is vital for decarbonising hard-to-abate sectors. How the hydrogen is produced also offers major benefits. For instance, smart and flexible operation of electrolysers (which break down water into hydrogen and oxygen) can provide a range of valuable services. Smart electrification of electrolysers can:

- harness synergies between hydrogen production and renewable generation by increasing production when generation is high and decreasing it when generation drops;

- provide balancing services to the power grid, and earn additional revenues for electrolysers;

- reduce congestion on transmission and distribution networks;

- reduce curtailment in renewable generation; and

- reduce peak loads on grids and peak demand from buildings or industries, especially when coupled with hydrogen storage and fuel cells.

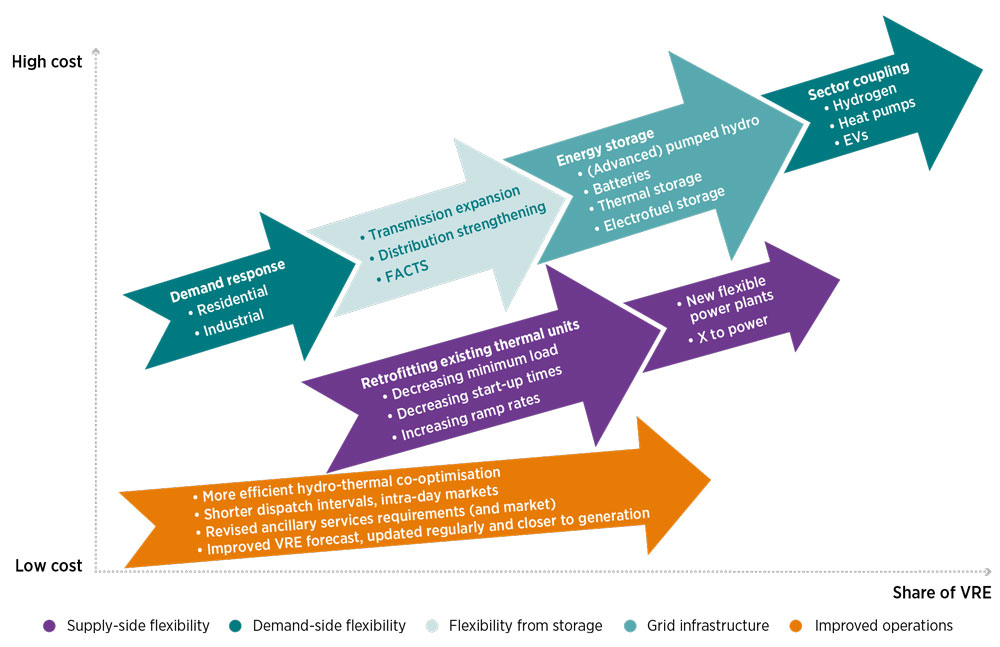

However, hydrogen should be viewed as a last resort option for providing flexibility, given that there are several low-cost alternatives available (see Figure 7.4).

FIGURE 7.4 Technical alternatives to increase system flexibility

Source: EV = electric vehicle; FACTS = flexible alternating current transmission system; VRE = variable renewable energy.