Geopolitics of the Energy Transformation

Summary for Policy makers

The ongoing energy transition is unprecedented due to its scale and the profound impact on the established socio-economic, technological, and geopolitical trends around the world. Renewables, in combination with energy efficiency, now form the leading edge of a far-reaching global energy transition. This transition is not a fuel replacement; it is a shift to a different system with commensurate political, technical, environmental, and economic disruptions. The central question this report addresses is whether and to what extent hydrogen exacerbates or mitigates these disruptions and in what ways.

Hydrogen, until now the missing piece of the clean energy puzzle, is likely to further disrupt energy value chains in coming years. The climate change imperative has been the main driver of the renewed policy focus on hydrogen. IRENA’s 1.5°C scenario envisages that clean hydrogen1 could meet up to 12% of final energy consumption by 2050. Majority of this would be produced using renewables, with the rest from gas and carbon capture and storage.

Hydrogen is likely to influence the geography of energy trade, further regionalising energy relations. With the costs of renewable energy falling, but those of transporting hydrogen high, the emerging geopolitical map is likely to show growing regionalisation in energy relations. Renewables can be deployed in every country, and renewable electricity can be exported to neighbouring countries via transmission cables. In addition, hydrogen can facilitate transport of the energy renewables produce over longer distances via pipelines and shipping, thus unlocking untapped renewable resources in remote locations. Some existing natural gas pipelines, with technical modification, could be repurposed to carry hydrogen.

Countries with an abundance of low-cost renewable power could become producers of green hydrogen, with commensurate geoeconomic and geopolitical consequences. Green hydrogen could be most economical in locations that have the optimal combination of abundant renewable resources, space for solar or wind farms, and access to water, along with the capability to export to large demand centres. New power nodes could arise in places that exploit these factors to become centres of hydrogen production and use.

The hydrogen business will be more competitive and less lucrative than oil and gas. Clean hydrogen will not generate returns comparable to those of oil and gas today. Hydrogen is a conversion, not an extraction business, and has the potential to be produced competitively in many places. This will limit the possibilities of capturing economic rents akin to those generated by fossil fuels, which today account for some 2% of global GDP. Moreover, as the costs of green hydrogen fall, new and diverse participants will enter the market, making hydrogen even more competitive.

Hydrogen trade and investment flows will spawn new patterns of interdependence and bring shifts in bilateral relations. A fast-growing array of bilateral deals indicates that these will be different from the hydrocarbon-based energy relationships of the 20th century. More than 30 countries and regions have hydrogen strategies that include import or export plans, indicating that cross-border hydrogen trade is set to grow considerably. Countries that have not traditionally traded energy are establishing bilateral relations centering on hydrogen-related technologies and molecules. As economic ties between countries change, so might their political dynamics.

Map source: Natural Earth, 2021

Notes: Information on this fgure is based on the information contained in government documents at the time of writing.

Disclaimer: This map is provided for illustration purposes only. Boundaries and names shown on this map do not imply any endorsement or acceptance by IRENA.

Hydrogen diplomacy is becoming a standard fixture of economic diplomacy in several countries. Access to hydrogen is often seen as an element of energy security, and overall national resilience, particularly for industries where other solutions are not feasible or uneconomical. Some countries that expect to be importers are already engaged in dedicated hydrogen diplomacy. Germany and Japan have been trailblazers, but other countries are following close behind them. Potential exporters are deploying similar strategies, with many including hydrogen – green hydrogen in particular – at the highest levels of their diplomacy.

Fossil-fuel exporters consider clean hydrogen an attractive way to diversify their economies. Many current exporters are pivoting to clean hydrogen to develop new export industries. They can leverage established energy infrastructure, a skilled workforce and existing energy trade relations. While blue hydrogen seems like a natural fit, many fossil-fuel producing countries have ample renewable potential to shift directly to the green variety as well. United Arab Emirates’ Hydrogen Leadership Roadmap is explicitly taking such dual approach, and several others are exploring this path including Australia, Oman and Saudi Arabia. Nevertheless, fossil-fuel producers should continue to develop broad-based economic transition strategies, given that hydrogen will not compensate for loss in revenues.

The technical potential to produce green electricity – and, in turn, large amounts of green hydrogen – exceeds estimated global demand by several orders of magnitude. Many countries have declared their ambition to become exporters of hydrogen, limiting the likelihood of export concentration. Judging by their strategies and growing bilateral deals, even net energy importers such as Chile, Morocco and Namibia seem poised to become green hydrogen exporters. However, the supply of hydrogen will be constrained by the pace of deployment of capital and cost of production, particularly where long-term markets are not assured.

Africa, the Americas, the Middle East and Oceania have the highest technical potential for green hydrogen production. The ability to produce large volumes of low-cost green hydrogen, however, varies widely. Countries will have to set their strategies in light of broader social and economic priorities, including the ability to decarbonise their energy systems or tackle energy access and poverty, currently prevailing in over 80 countries worldwide. Having access to abundant renewables is an asset in the clean hydrogen race, but it might not be enough. Many other factors come into play, including existing infrastructure and the current energy mix, along with the cost of capital and access to necessary technologies. Whether the technical potential can be realised will also depend on soft factors like government support, the investment climate and political stability.

Higher project finance costs do not necessarily impede investment in countries with higher risk profiles. The upstream oil and gas sectors show that where revenue potential is sufficient, investment will flow in despite country risk. The same should apply to countries showing a low-cost potential for green hydrogen. There are limits, of course. Countries in turmoil, some of which have great potential, are unlikely to be able to realise investment opportunities owing to the immense risks of doing business in such locations.

The 2020s could become the era of a big race for technology leadership, as costs are likely to fall sharply with learning and scaling-up of needed infrastructure. The geopolitics of clean hydrogen is likely to play out in several stages. Green hydrogen is projected to start competing with blue on cost by the end of this decade. This seems likely to occur sooner in countries such as China (thanks to its low-cost electrolysers), or Brazil and India (with cheap renewables and relatively high gas prices). Green hydrogen was already more affordable than grey across Europe during the 2021 spike in natural gas prices. But the uptake will greatly depend on predictable demand, especially in harder to abate sectors where no alternatives exist.

Sources: IRENA (forthcoming-b).

Cross-border trading of hydrogen will increase in the 2030s, at pace with the cost-competitiveness of green hydrogen. Across many decarbonisation scenarios, demand starts to take off from 2035. IRENA envisages that two-thirds of green hydrogen production in 2050 would be used locally, and one-third traded across borders. Pipelines, including adapted natural gas pipelines, are likely to facilitate half of this trade. The other half would be loaded on ships in the form of hydrogen derivatives, notably ammonia.

In the short to medium term, countries and regions can assert technology leadership and shape the rules of the growing market. Having a stake in the hydrogen value chain can boost economic competitiveness. The direct economic stakes are high, and the market potential is considerable. In the long run, countries with ample renewable potential could become sites of green industrialisation, using their potential to attract energy-intensive industries.

Equipment manufacturing offers an opportunity to capture value in the coming years and decades. The hydrogen value chain is extensive, and the bulk of investment will be needed for renewable power. Along this value chain, estimates point to a USD 50-60 billion market potential for electrolysers and a USD 21-25 billion market for fuel cells by the middle of the century. China, Europe and Japan have developed a strong head start in producing and selling electrolysers, but the market is still nascent and relatively small. Innovation and emerging technologies can change the current manufacturing landscape.

Any form of hydrogen may strengthen energy independence and resilience, but most of the benefits stand to come from green hydrogen. Today, there are three main ways in which hydrogen can bolster energy security: 1) by reducing import dependence, 2) by mitigating price volatility and 3) by boosting the flexibility and resilience of the energy system, through diversification. Most of these benefits are associated with green hydrogen. Conversely, blue hydrogen would follow the patterns of gas markets, resulting in import dependencies and market volatilities. Moreover, the expected cost reduction in green hydrogen means that investments in supply chains based on fossil fuels – especially assets planned to stay in operation for many years – may end up stranded.

The raw materials needed for hydrogen and renewable energy technologies are likely to draw more attention to material security. While geological supplies for most minerals and metals are presently sufficient, markets could become very tight owing to rapidly rising demand, and the long lead times of mining and refining projects. A relatively small shift in supply or demand can cause significant price fluctuations. Such fluctuations could reverberate through hydrogen supply chains and affect the overall cost of equipment, along with the revenues of miners and exporters of raw materials. Supply chain problems caused by COVID-19 are also instructive when considering possible risks beyond those already well-known.

Hydrogen trade flows are unlikely to become weaponised or cartelised. This is because hydrogen can be produced from many primary energy sources and in a wide variety of places worldwide. Indeed, it is a manufactured product rather than a raw material or energy source. Therefore, green energy trade flows are unlikely to lend themselves as easily to geopolitical influence as oil and gas. That said, supply shortages could arise, particularly in the early years of hydrogen trade, when the number of suppliers is limited and most trade is still governed by bilateral arrangements.

Shaping the rules, standards and governance for hydrogen trade will have a significant impact in determining which technologies dominate future markets. The success of clean hydrogen markets hinges upon the ability to set coherent and transparent rules, standards and norms to facilitate its deployment across countries, regions and sectors. Standards are designed to improve the quality, safety, and interoperability of various goods and services. At the same time, divergent standards could slow down progress and lead to market fragmentation, stir regulatory competition, and erect trade barriers. Setting standards could be an arena for geopolitical competition or international co-operation. Ultimately, all players can gain from a coherent and transparent global system.

Certificates of origin rooted in a transparent and credible international system will be needed to monitor and manage hydrogen’s contribution to climate change efforts. Transparency in how emissions are measured will be essential. There are well-known risks of carbon lock-in if hydrogen strategies prolong fossil fuel use and hinder energy efficiency and electrification. Robust and well-thought-out policy frameworks can help ensure that hydrogen effectively contributes to reducing greenhouse gas emissions.

Price transparency early on would support the rapid evolution of the global market in hydrogen. The currencies and pricing mechanisms that take hold in the emerging market are likely to have considerable geopolitical effects. The currency chosen will be positioned to become a global benchmark as the market expands. Those associated with that currency will to some degree be sheltered from exposure due to fluctuating import costs. For instance, the European Union, likely to become one of the key import markets, seeks to denominate its future hydrogen imports in euros. Moreover, putting a price on carbon might be helpful, or even necessary, to make green hydrogen competitive with the grey variant and, ultimately, with fossil fuels. In that sense, hydrogen may become embroiled in a broader set of carbon trade wars.

Investment decisions are long-lived and the risks of stranded assets high, so fixed infrastructure should be assessed with a long-term logic. Every investment and planning decision around energy infrastructure today should consider that the geography of a decarbonised economy is likely to be very different from what currently makes sense. Significant electrification of end uses will reshape demand. On the supply side, renewable hydrogen production will likely occur in locations other than today’s oil and gas fields. While some of the existing infrastructure could be repurposed, the technical challenges and economic costs of such repurposing should be accounted for from the outset.

Helping developing countries deploy hydrogen technologies early on could improve energy security for all, while preventing the global decarbonisation divide from widening. A diverse hydrogen market would reduce supply chain risks and improve energy security for all. Access to technology, training, capacity building and affordable finance will be key to realising the full potential of hydrogen to decarbonise the global energy system and contribute to global stability and equity. Establishing hydrogen trade relations could open new possibilities to set up local hydrogen value chains, stimulate green industries and create jobs in countries rich in renewables.

Global efforts should focus on the applications that provide the most immediate advantages and enable economies of scale, particularly in the coming years. Prioritising high-demand applications for which hydrogen is the best — and perhaps the only — alternative is more likely to be cost-effective and less susceptible to the risks of nascent markets. One example could be supporting and then accelerating a shift to green hydrogen in industrial applications where hydrogen is already used, such as refining and the production of ammonia and methanol.

Depending on how it is developed, hydrogen could have both positive and negative effects on sustainable development. The concept of “human security” is often used to describe the root causes of geopolitical instability to account for threats such as climate change, poverty and disease, which can undermine peace and stability within and between countries. Going forward, it will be important to gain greater understanding of the multidimensional nature of global threats and vulnerabilities to foresee and defuse certain risks that may come with the deployment of hydrogen on a major scale.

1.1 The dawn of clean hydrogen

In recent years, hydrogen has risen up the agenda as a potential missing piece of the clean energy puzzle. A growing number of countries now have a national hydrogen roadmap or strategy, and a sizeable portion of the COVID-19 stimulus and recovery funds have been dedicated to the acceleration of hydrogen. At the 2021 United Nations Climate Change Conference (COP26) in Glasgow, 32 countries and the European Union (EU) agreed to work together to accelerate the development and deployment of clean hydrogen (Box 1.1) and ensure that “affordable renewable and low-carbon hydrogen is globally available by 2030” (UNFCCC, 2021).

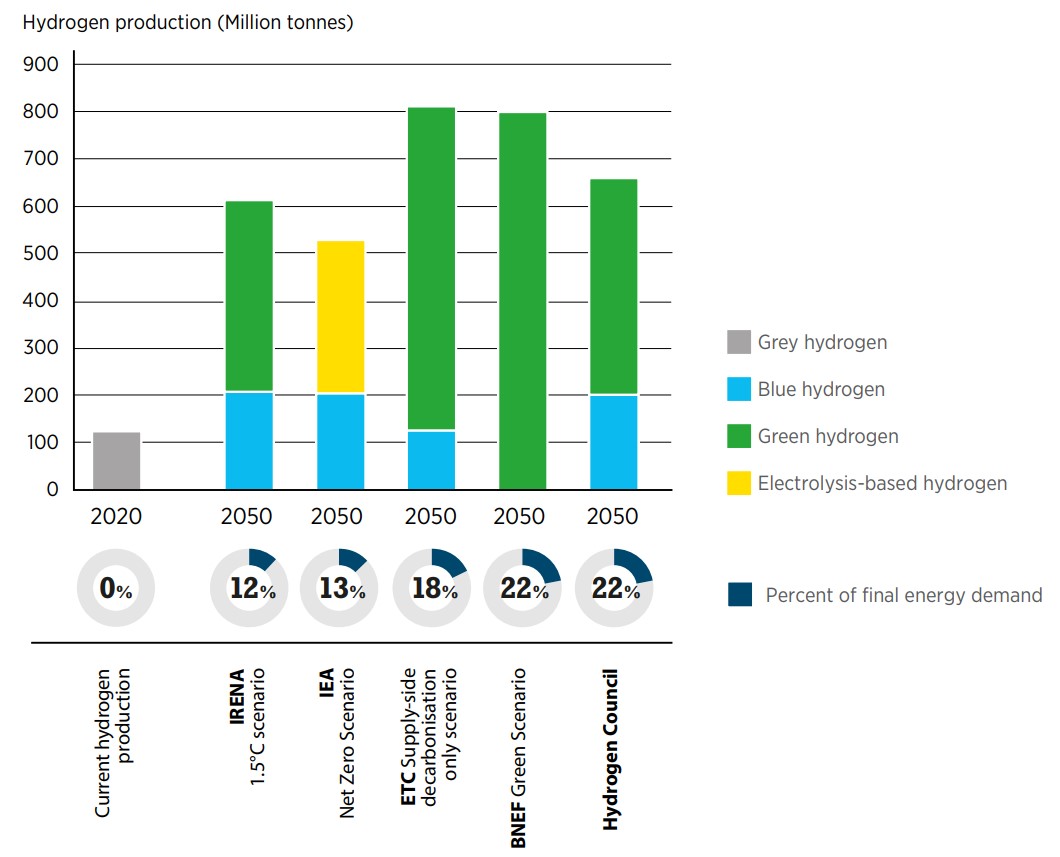

Hydrogen has spurred multiple waves of interest in the past without significant impact. Two factors make this time different. First, governments worldwide have rallied behind the target of net zero emissions by the middle of this century (Black et al., 2021). Having a reasonable chance of limiting global temperature rise to 1.5°C, the goal laid out in the 2015 Paris Agreement, requires reaching net zero emissions by 2050 (IPCC, 2021). To do so, all sectors of the economy need to cut their emissions, including heavy industry and long-haul transport, where limited solutions exist. Hydrogen has emerged as a key option for reducing emissions in these sectors. Second, the plummeting costs of renewables and electrolysers are improving the economic attractiveness of "green" hydrogen – that is, hydrogen produced through the electrolysis of water powered by renewable electricity. The increasing share of variable renewables, such as wind and photovoltaic (PV) solar power, also creates demand for flexibility and storage, which hydrogen can help deliver. Green hydrogen can thus complement and extend the ongoing revolution in renewable electricity. As a result of these factors, hydrogen and hydrogen-based fuels are now projected to meet a sizeable share of final energy demand in 2050, up from virtually nothing today (Figure 1.1). In all of these projections, current “grey” hydrogen production (based on fossil fuels) is completely phased out, and green hydrogen is the dominant production pathway, complemented by “blue” hydrogen, which is based on fossil fuels with carbon capture and storage (CCS).

BOX 1.1 Key terms used in this report

- Clean hydrogen refers to both green hydrogen and blue hydrogen. Although both types may play a role in the energy transition, for the purpose of this report, blue hydrogen was conceptualised as “clean” where methane emissions are extremely low and with very high carbon capture rates.

- Low-carbon hydrogen refers to blue hydrogen that does not meet the emission standards above and to hydrogen made with grid-powered electrolysis where the grid is not decarbonised.

- Hydrogen derivatives refer to the downstream molecules into which hydrogen can be converted (e.g. ammonia, methanol, synthetic fuels). When these products are produced with hydrogen from electrolysis, they are known as “Power-to-X” products.

- Synthetic fuels refer to a variety of gaseous and liquid fuels produced from hydrogen and carbon, including synthetic kerosene, synthetic diesel and others. When hydrogen is produced by electrolysis, these fuels are also referred to as “powerfuels” or “e-fuels”. They can be used as “dropin” fuels, as they can be used in conventional engines and fuel supply infrastructure.

Hydrogen has spurred multiple waves of interest in the past without significant impact. Two factors make this time different. First, governments worldwide have rallied behind the target of net zero emissions by the middle of this century (Black et al., 2021). Having a reasonable chance of limiting global temperature rise to 1.5°C, the goal laid out in the 2015 Paris Agreement, requires reaching net zero emissions by 2050 (IPCC, 2021). To do so, all sectors of the economy need to cut their emissions, including heavy industry and long-haul transport, where limited solutions exist. Hydrogen has emerged as a key option for reducing emissions in these sectors.

Second, the plummeting costs of renewables and electrolysers are improving the economic attractiveness of "green" hydrogen – that is, hydrogen produced through the electrolysis of water powered by renewable electricity. The increasing share of variable renewables, such as wind and photovoltaic (PV) solar power, also creates demand for flexibility and storage, which hydrogen can help deliver. Green hydrogen can thus complement and extend the ongoing revolution in renewable electricity.

As a result of these factors, hydrogen and hydrogen-based fuels are now projected to meet a sizeable share of final energy demand in 2050, up from virtually nothing today (Figure 1.1). In all of these projections, current “grey” hydrogen production (based on fossil fuels) is completely phased out, and green hydrogen is the dominant production pathway, complemented by “blue” hydrogen, which is based on fossil fuels with carbon capture and storage (CCS).

Figure 1.1 Estimates for global hydrogen demand in 2050

Notes: The International Energy Agency refers to “fossil-based with CCUS” (carbon capture, utilisation and storage) and “electrolysis-based” hydrogen. The Hydrogen Council projects that 60-80% of hydrogen production will be renewables based, with the rest “low-carbon”, which it defines as “hydrogen produced from energy sources of non-renewable origin with a carbon footprint below a defined threshold”. Current hydrogen production includes hydrogen created as byproduct from other processes.

1.2 Geopolitical significance of clean hydrogen

Building up global clean hydrogen value chains will bring geoeconomic and geopolitical shifts. Most notably, green hydrogen is emerging as a potential game changer for reducing emissions and achieving climate neutrality without stymying economic and social development.

The economic stakes are high. Current annual hydrogen sales represent a market value of approximately USD 174 billion, which already exceeds the value of annual trade in liquefied natural gas (LNG).2 Even if hydrogen’s use is limited to industrial processes and long-distance transport, its market potential is enormous. A single steel plant using hydrogen rather than fossil fuel to reduce iron would utilise about300 000 tonnes of hydrogen annually, absorbing the output of 5 gigawatts (GW) of electrolysers (Mission Possible Partnership, 2021). Global electrolyser capacity today stands at just over 0.3 GW. According to major investment banks, by 2050, global sales of hydrogen could be worth USD 600 billion (Financial Times, 2021), and the value chains of green hydrogen could become a USD 11.7 trillion investment opportunity over the next 30 years,3 covering everything from dedicated renewable capacity and electrolysers, to transport infrastructure (Goldman Sachs, 2020).

Hydrogen’s transformative reach goes beyond its estimated market value. It is best thought of as a general-purpose energy carrier that can foster innovation across many different industries and sectors. Its geopolitical impact might follow the patterns of steam power, electricity, or the internal combustion engine. Each in their own way, these technologies have transformed the machines and fuels on which much of our modern civilization runs. In the process, they have also affected different aspects of human life, altered global trade patterns, and shaped the global balance of power. While these technologies have brought many benefits to humankind, the benefits have not been fairly distributed. They have therefore saddled societies with new externalities and global challenges.

Compared to these epoch-defining technologies, clean hydrogen’s impact will likely be smaller, but it should not be brushed aside too quickly. Behind the simple chemical formula of hydrogen gas (H2), lies an entire system of infrastructure to produce, transport, convert and use hydrogen. Such a system could create new connections between the previously separated energy sectors of power, heat, and mobility. It could foster partnerships that transcend traditional industry boundaries. More importantly, the push to develop clean hydrogen as a major energy carrier is likely to disrupt current energy value chains and create opportunities for more countries to play a significant role. Eventually, it might even lead to an entirely new economic geography of industrial activity.

The geopolitics of clean hydrogen is likely to play out in different stages. The 2020s could be the era of the big race for technology leadership, with costs falling significantly and rapid scaling up of the required infrastructure. In many locations, green hydrogen is set to compete on costs with blue by 2030 (IRENA, 2020a). Across many decarbonisation scenarios, demand starts to take off from 2035 (World Energy Council, 2021). During this period, international trade of hydrogen and derivatives could grow significantly, although initial trading routes might be established earlier (Ram et al., 2020).

1.3 Objectives of the report

This report provides a comprehensive analysis of the geopolitical drivers and potential consequences of the development of clean hydrogen value chains.

A central theme around which this report is built is the concept of ‘disruption’. We are witnessing transformations in many aspects of economies and societies, ranging from energy systems, climate change, technological trajectories, geopolitical relationships, and trade and investment. Given the turbulence of political, technical, environmental, and economic systems, the central question this report addresses is whether, and to what extent, hydrogen exacerbates or mitigates these disruptions, and who benefits or may be disadvantaged by these developments. The goal of this report is not only to describe how hydrogen can disrupt future energy systems, but also offer insights into how countries and stakeholders can prepare for positive or negative disruptions.

The possible pathway on which clean hydrogen might evolve still involves many uncertainties. This report is therefore a horizon scanning exercise that is exploratory in nature. The 1.5°C scenario of the International Renewable Energy Agency (IRENA), as depicted in the Agency’s World Energy Transitions Outlook (WETO), is used as a baseline for the analysis (Box 1.2) (IRENA, 2021a). However, this report focuses not only on the geopolitical implications of a defined hydrogen pathway, but also on the ways in which different actors are actively trying to shape multiple potential pathways for the development of hydrogen.

Two surveys were conducted to inform the analysis in this report (Box 2.2). One polled IRENA Members,4 the other a group of topical experts. The report also draws on the substantial body of work that IRENA has already carried out on hydrogen and related topics, from technical, economic and policy perspectives. It further draws on the work of experts worldwide, including those participating in IRENA’s Collaborative Framework on the Geopolitics of Energy Transformation.

This report reflects on many of the key themes covered by the 2019 Global Commission report (IRENA, 2019a), including technology leadership, energy security and shifting trade patterns, among others. It outlines policy considerations for governments and other actors to help mitigate the geopolitical risks and capitalise on opportunities.

BOX 1.2 KEY PROJECTIONS OF HYDROGEN USE BY 2050 IN IRENA’S 1.5°C SCENARIO

- Hydrogen and its derivatives account for 12% of final energy use and 10% of carbon dioxide (CO2) emissions reductions. They play an important role in harder-to-decarbonise, energy-intensive sectors like steel, chemicals, long-haul transport, shipping and aviation. Hydrogen also helps balance the supply of and demand for renewable electricity and serves as long-term seasonal storage.

- Some 5 000 GW of hydrogen electrolyser capacity are needed, up from just 0.3 GW today.

- The electricity demand to produce hydrogen reaches close to 21 000 terawatt hours (TWh), almost the level of global electricity consumption today.

- The production of green hydrogen and its derivatives will use 30% of the total electricity demand in 2050.

- At least two-thirds of total production is green hydrogen, with the rest coming from blue hydrogen.

2.1 What is hydrogen?

Hydrogen is the oldest, lightest and most abundant element in the universe. It is naturally present in many compounds, including water and fossil fuels.

Hydrogen gas is used mainly as a feedstock for the (petro)chemical industry: crude oil refining, ammonia synthesis (primarily for fertiliser production) and methanol production for a wide variety of products (including plastics).

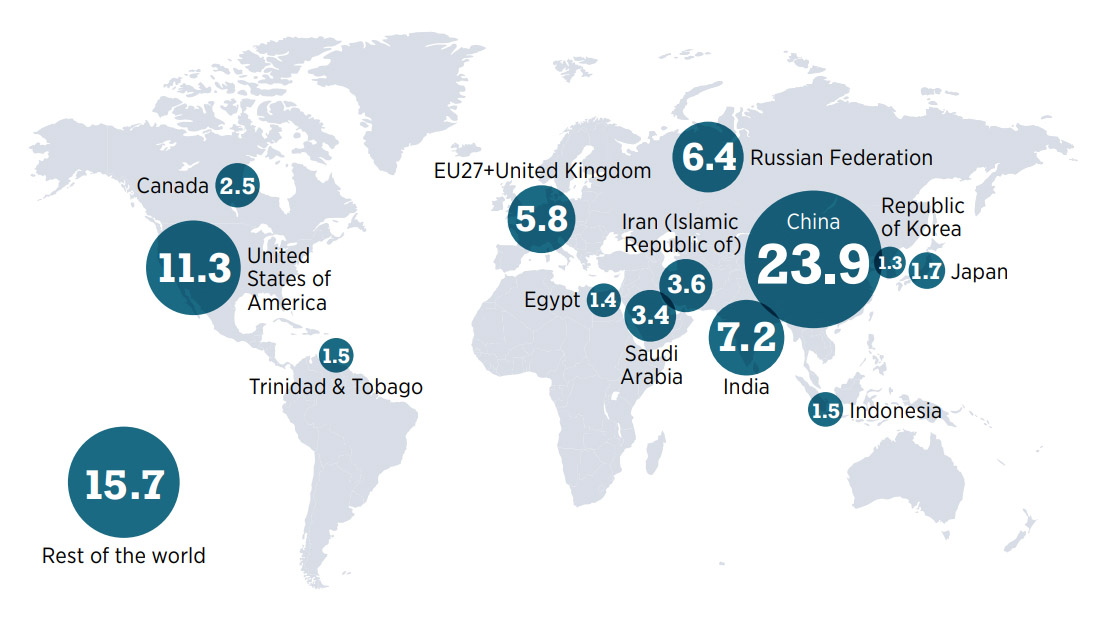

Around 120 million tonnes of hydrogen is produced globally, twothirds of which is pure hydrogen and one-third of which is a mixture with other gases (IEA, 2019a). China is the world’s largest producer and consumer of hydrogen (Figure 2.1). It produces almost 24 million tonnes of pure hydrogen per year, accounting for nearly one-third of dedicated global production.

Hydrogen can also be used as a fuel. When burned, it can generate heat of more than 1 000°C without emitting CO2.5 Further, hydrogen can also be used in fuel cells, where it chemically reacts with oxygen to produce electricity without emitting any pollutants or greenhouse gases. The only by-product of this chemical reaction is water vapour.

Figure 2.1 Hydrogen consumption in 2020 (million tonnes per year)

Note: Values are derived from current production of ammonia, methanol, refining and direct reduced iron for steel.

Disclaimer: This map is provided for illustration purposes only. Boundaries and names shown on this map do not imply any endorsement or acceptance by IRENA.

2.2 Main production pathways

Despite its abundance on Earth, hydrogen does not exist naturally in its pure form in large quantities. There are no vast deposits of hydrogen in the ground that can be extracted.6 Hydrogen is found almost exclusively in compounds, notably water molecules (hydrogen and oxygen) and fossil fuels (hydrogen and carbon). Hydrogen can be released from these compounds, but doing so requires energy.

A colour-code system is commonly used to refer to different hydrogen production methods (Figure 2.2). Most hydrogen today is grey hydrogen, which is produced using fossil fuels, notably through steam methane reforming of natural gas or gasification of coal.7 These fossil fuel-based production methods, which account for 95% of today’s hydrogen supply, result in a substantial CO2 footprint and are not compatible with moving towards net zero emissions.

Two main routes are under consideration to replace grey hydrogen with a clean form of production: green and blue hydrogen. Green hydrogen production is fully consistent with the net zero route. It relies on technologies that have long been well known, based on water electrolysis (Box 2.1) powered by renewable electricity. Currently, hydrogen production from renewable sources is limited, but this is set to change with the global focus on its potential.

Blue hydrogen is produced from fossil fuels with CCS. Retrofitting CCS to grey hydrogen production facilities would allow continued use of these assets with lower greenhouse gas emissions. However, blue hydrogen relies on fossil gas, which brings risks of upstream or midstream leakages of methane, a much more potent greenhouse gas than CO2. Blue hydrogen can thus yield very low greenhouse gas emissions, only if methane leakage emissions do not exceed 0.2%,8 with close to 100% carbon capture. Such rates are still to be demonstrated at scale (Bauer et al., 2021; Howarth and Jacobson, 2021; IEA, 2021b; IRENA, 2020b; Saunois et al., 2016).

Blue hydrogen has other limitations that have restricted its deployment. It uses fossil fuels, exposing it to price fluctuations, such as the price spike in late 2021 in many parts of the world, notably Asia and Europe (Collins, 2021a), and does not support the goals of climate resilience or energy security. It also adds CO2 transport and storage costs and requires monitoring of stored CO2.

However, if blue hydrogen meets strict emissions criteria, it could play an important role in scaling up hydrogen volumes in the short-to-medium term and drive the development of related infrastructure and technologies along the value chain. Moreover, blue hydrogen could offer additional flexibility in the hydrogen market. In the long run, however, green hydrogen is a zero-carbon solution and should therefore be the endgame.

Other low-carbon pathways for hydrogen production exist. One option is “turquoise” hydrogen, which relies on pyrolysis of methane (natural gas), which does not emit CO2. The only by-product of this process is the solid material “carbon black”, for which there is an existing market, albeit a relatively small one. Another option is “pink” hydrogen, from nuclear electricity. A third is biomass gasification with CCS, which can result in negative CO2 emissions. None of these types of hydrogen is included in this report, which gives priority to more developed production methods.

BOX 2.1 What is an electrolyser?

Electrolysis is the chemical process that produces hydrogen from water and electricity. Electrolysers – devices that can split water into oxygen and hydrogen – were invented over 200 years ago.

Multiple water electrolyser technologies exist. Four of them hold promise: alkaline, proton exchange membrane (PEM), solid oxide electrolyser cells (SOEC) and anion exchange membrane (AEM). All of the installed electrolyser capacity uses either alkaline or PEM technologies. AEM electrolysers are still relatively new and have limited deployment; their potential advantages lie in the fact that they use no precious metals and use a membrane that is less expensive than that used for PEM.

Table 2.1 Main electrolyser technology comparison

| Type | Commercial Status | Considerations |

|---|---|---|

| Alkaline | Mature |

|

| Proton exchange membrane(PEM) | Commercial, fast growth |

|

| Solid oxide electrolyser cells (SOEC) | Demonstration plants |

|

| Anion exchange membrane (AEM) | Limited deployment |

|

2.3 Hydrogen applications and priority setting

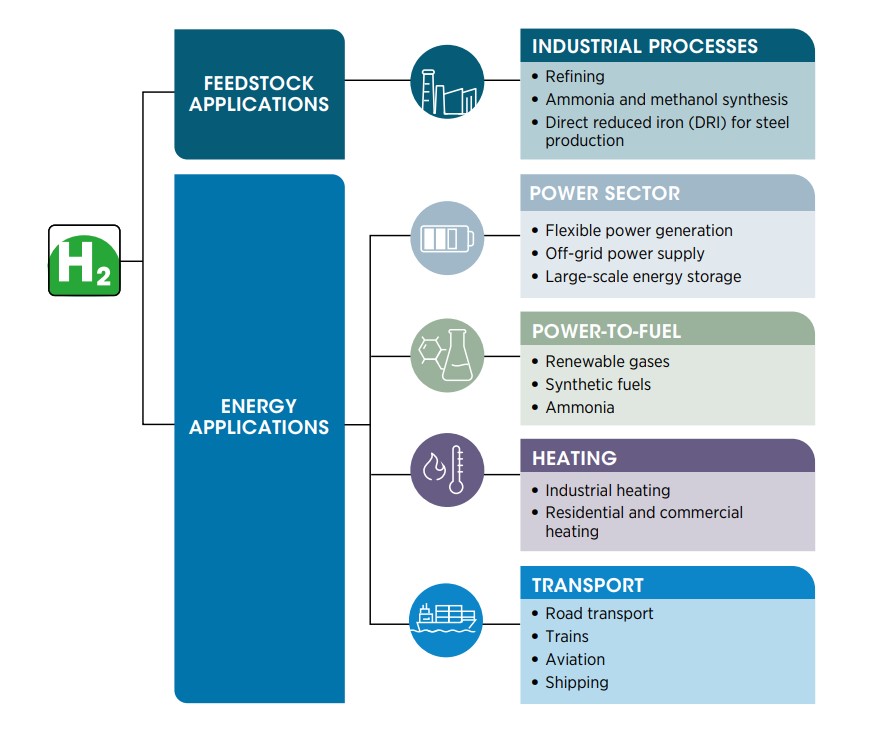

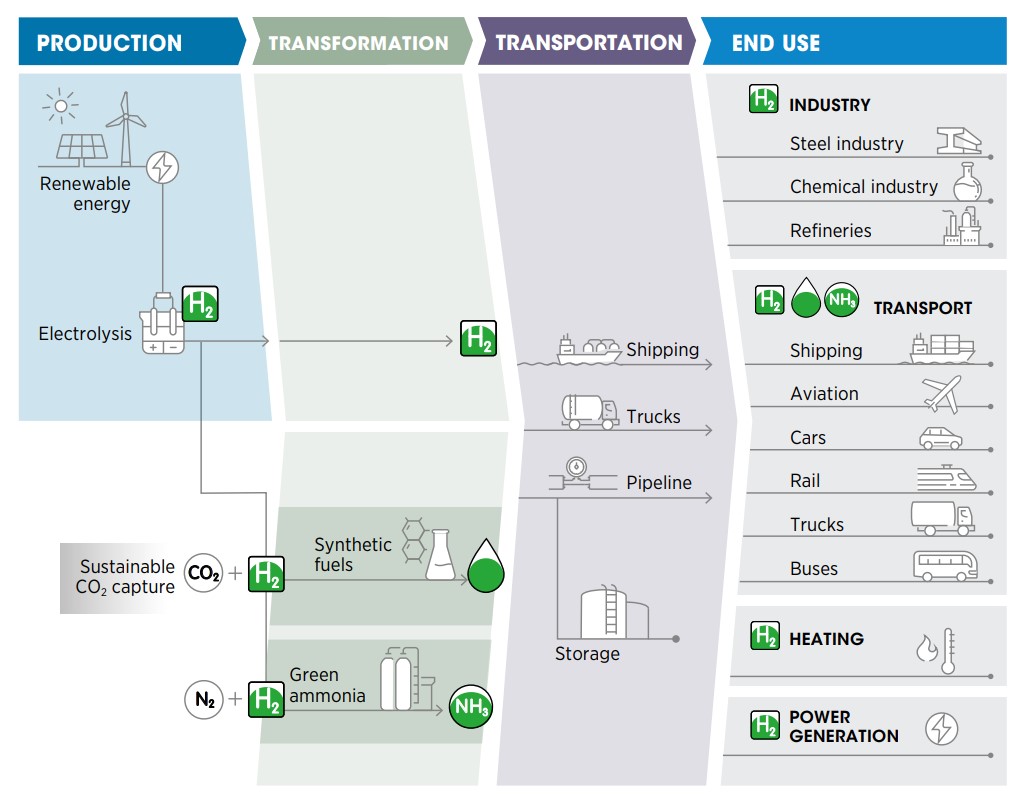

Hydrogen is a versatile energy carrier that can be used in many applications. Figure 2.3 shows the potential uses for hydrogen, some of which can provide early demand for hydrogen and help the industry take off.

Figure 2.3 Potential uses for clean hydrogen

Decarbonisation strategies require careful management to ensure that the technologies and solutions selected are most efficiently deployed. Thus, the wide array of options calls for identification of uses in which hydrogen can provide the most value. Its production, transport and conversion require energy, raising overall demand. Indiscriminate use can slow the energy transition, also diluting the decarbonisation efforts of the power generation sector. Hydrogen is therefore best reserved for the uses that currently have no viable alternative. Figure 2.4 compares possible end uses based on the size of application and the maturity of hydrogen solutions compared with electricity-based ones. Policy attention should be given to the more mature and centralised hydrogen solutions. This attention can involve dedicated research, planning and supporting policies (IRENA, forthcoming-b).

Making the shift to a truly sustainable economy is not simply about switching energy sources and keeping the current energy system; more efficient, just and equitable ways of using energy must be developed. Doing so involves reducing unnecessary energy consumption across many final uses and changing the current economic system, which is based on continuously increasing consumption. In heavy industry, for example, 40% of CO2 emissions could be saved by reusing steel, aluminium and plastics more effectively (Lovins, 2021a). Another example would be a modal shift from short-distance flights to electrified trains, where possible, to reduce demand

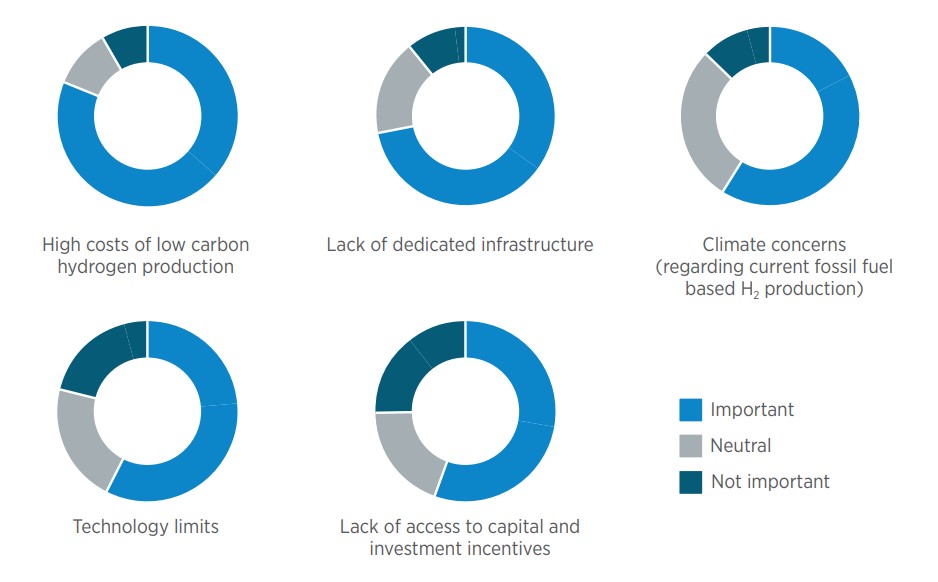

2.4 Barriers to scaling up hydrogen

The following barriers currently prevent clean hydrogen from making a larger contribution to the energytransformation:

- Cost: The cost of clean hydrogen, particular green hydrogen, is still high relative to high-carbon fuels. Not only the cost of production but the costs of transporting, converting and storing hydrogen are also high. Adopting clean hydrogen technologies for end uses can be expensive and CCS is yet to be deployed at scale.

- Technological maturity: Some technologies in the hydrogen value chain required for decarbonisation still have a low level of technological readiness and need to be proven at scale. For instance, gas turbines that operate exclusively with hydrogen are not currently available off the shelf, and when it comes to maritime trade, there is only one prototype vessel that can transport liquid hydrogen.

- Efficiency: Hydrogen production and conversion incur significant energy losses at each stage of the value chain, including production, transport, conversion and use. Moreover, production of blue hydrogen is energy-intensive, adding to overall energy demand.

- Sufficient renewable electricity: By 2050, the production of hydrogen with electrolysers may consume close to 21000 TWh – almost as much electricity as is produced globally today (IRENA, 2021a). As more end-use sectors are electrified, a lack of sufficient renewable electricity may become a bottleneck for green hydrogen.

- Policy and regulatory uncertainty: Although over 140 countries have pledged to achieve net zero emissions within the coming decades, the speed with which these goals will be achieved remains uncertain. Stable, long-term policy frameworks are needed to support development and deployment at scale.

- Standards and certification: Countries lack institutionalised mechanisms to track the production and consumption of any shade of hydrogen and identify its characteristics (e.g. origin and life-cycle emissions) (IRENA, 2020b; IRENA, IEA and REN21, 2020).9 Moreover, hydrogen is not counted in official statistics of total final energy consumption and the economic value of clean hydrogen’s contribution to emission reductions is not recognised.

- Chicken-and-egg problem: There is a chicken-and-egg problem in building out the necessary infrastructure for hydrogen. Without demand, investments remain too risky for wide-scale production that could reduce costs, but without economies of scale the technology remains too costly.

Figure 2.5 Main perceived barriers to develop hydrogen policies and strategies

BOX 2.2 Geopolitics of hydrogen surveys

For an emerging and rapidly evolving topic that has gathered widespread interest, two voluntary surveys were designed to garner feedback from policy makers and industry experts to provide a baseline for observing hydrogen sector developments.

The first survey was focused on gathering input from countries to develop a high-level understanding of country plans and associated drivers and barriers of hydrogen’s role in the energy transition. The survey was issued to IRENA’s Membership, 164 countries and the EU at the time. A total of 48 responses from 37 Members were received.

A second survey was issued to target topical experts (purposive sampling) to gather more technical views. Under this second survey, 162 experts were approached, and 78 responses received. Input received was analysed and aggregated. Selected outputs are provided throughout this report. The full survey results are available in a digital annex.

2.5 Prospects for international hydrogen trade

Today, hydrogen is a very local business. About 85% of hydrogen gas is produced and consumed on-site within a facility rather than bought and sold on the wider market (IEA, 2019a). Even where hydrogen is sold, it is usually not transported across large distances because of the logistical difficulties and costs.

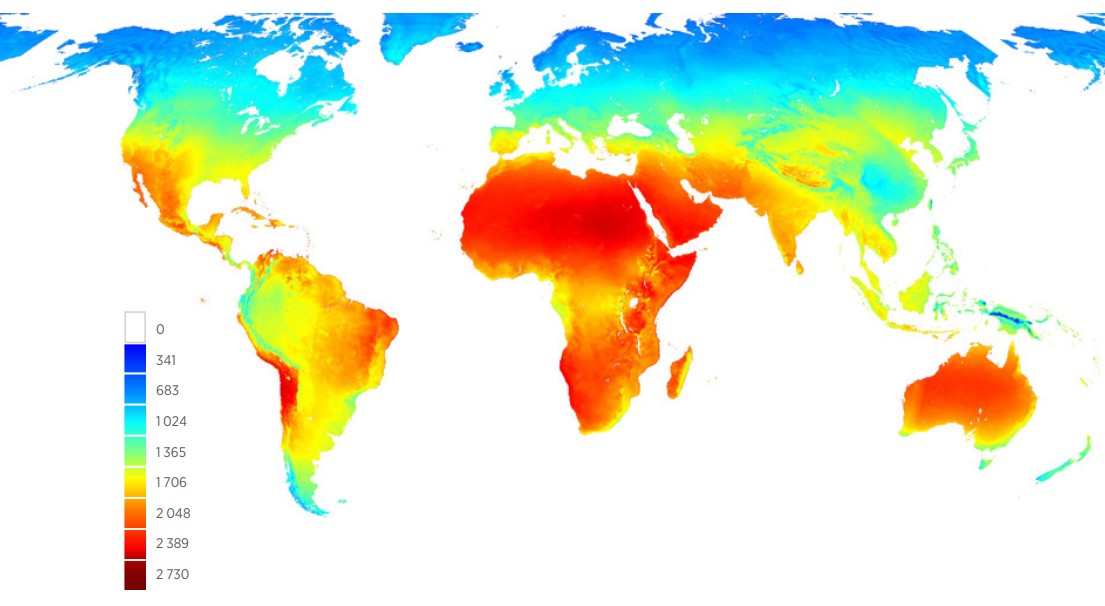

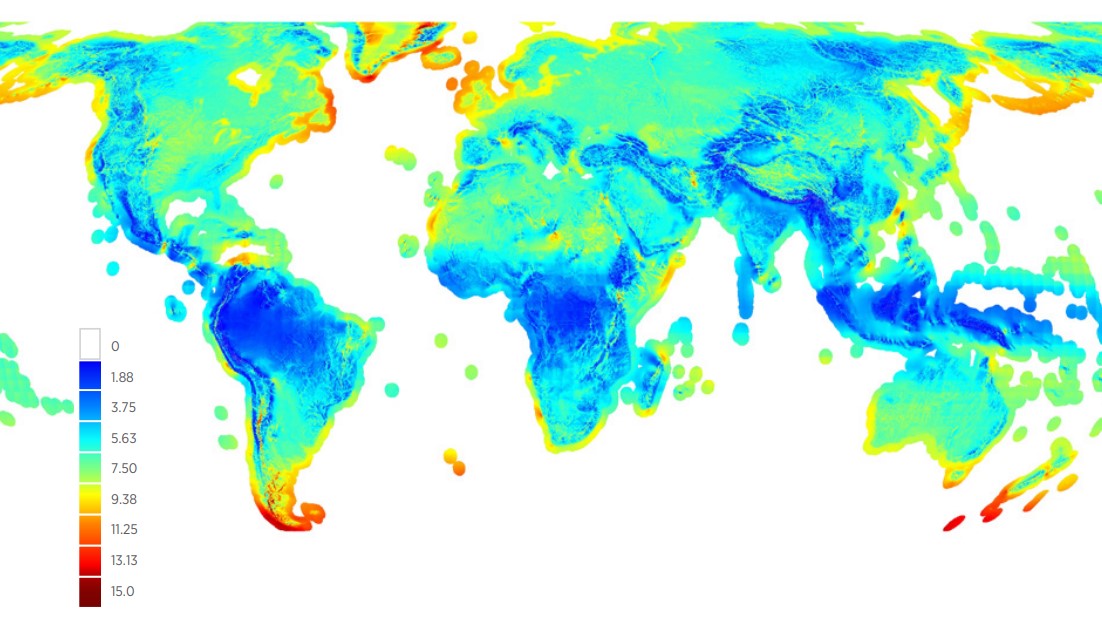

Over time, hydrogen could become an internationally traded commodity. The green variety offers additional means to “ship sunshine”, that is, transport solar and other renewables across borders. The single-largest cost component of producing green hydrogen is the cost of electricity (IRENA, 2020a). As the levelised cost of renewables differs significantly across regions, the price of hydrogen will also differ.10 Green hydrogen will be most economically produced in locations that have an optimal combination of abundant renewable resources (Figure 2.6 and Figure 2.7), available land, access to water and the ability to transport and export energy to large demand centres.

Figure 2.6 World solar technical potential

Note: Annual average global horizontal irradiation (kWh/m2). Also available on the IRENA Global Atlas for Renewable Energy web platform.

Disclaimer: This map is provided for illustration purposes only. Boundaries shown on this map do not imply any endorsement or acceptance by IRENA.

Figure 2.7 World wind technical potential

Note: Annual average wind speed at 100 metres (m/s). Also available on the IRENA Global Atlas for Renewable Energy web platform.

Disclaimer: This map is provided for illustration purposes only. Boundaries shown on this map do not imply any endorsement or acceptance by IRENA.

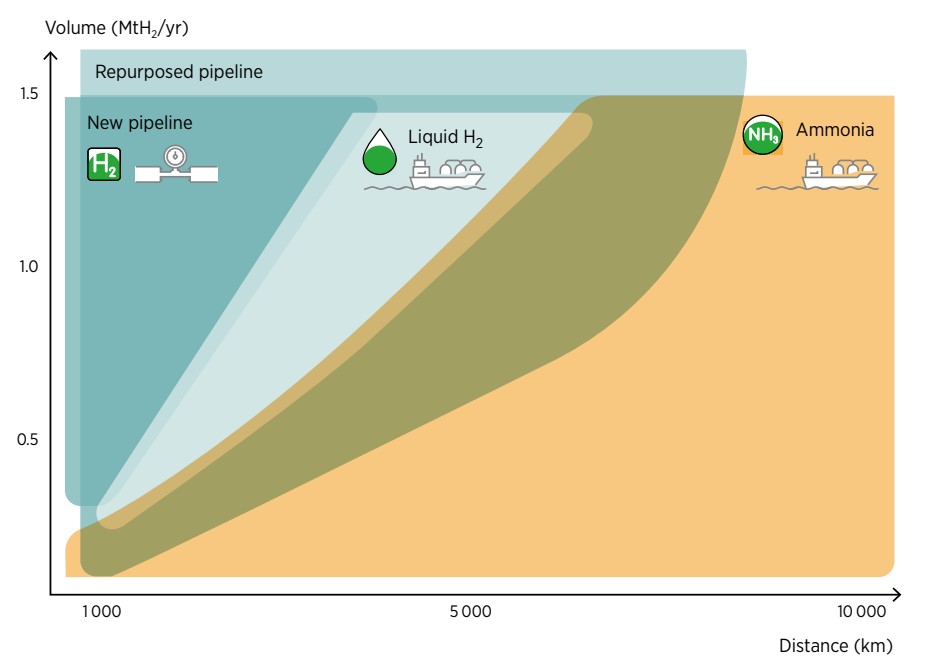

There are two main modes for transporting hydrogen across borders: pipelines and ships.11 Distance and volume determine which mode is cheapest (Figure 2.8). For instance, with small volumes (e.g. 0.3 million tonnes of hydrogen per year), pipelines could be cheaper than ships for distances below 1 500 km. For large volumes (e.g. 1.5 million tonnes of hydrogen per year), newly built hydrogen pipelines would be the most cost-effective option for distances up to 4 000 km. In cases where repurposed natural gas pipelines are an option,12 the cost effective range extends to 8 000 km. To put some of these distances into perspective, connecting Windhoek, Namibia to Johannesburg, South Africa, would require a pipeline of about 1 500 km. Connecting Toronto, Canada to Mexico City, Mexico would require a pipeline of about 4 000 km. Shipping from Chile to Japan is almost 17 000 km.

Figure 2.8 Cost efficiency of transport options when considering volume and distance

Note: H2 = hydrogen gas; km = kilometre. MtH2/yr = million tonnes of hydrogen per year.

There are about 4 600 km of dedicated hydrogen transmission pipelines operating in north-western Europe, the Russian Federation (Russia) and the United States of America (United States). Plans are in the making for trunk pipeline systems in Europe, called the “hydrogen backbone” (Gas for Climate, 2021a). It is also possible to simply transmit renewable electricity via cables and transform it into hydrogen at the end of the line. Whether a pipeline or a cable is the optimal solution depends on several factors, including the desired end product, the topography of the terrain, and the distance.

Hydrogen transport by ship is technically possible for larger distances where pipelines are not an option. Because of its low energy density by volume,13 gaseous hydrogen is best converted into a more energydense liquid before being loaded onto a ship. There are several vectors for hydrogen transport via ship (Box 2.3), but ammonia is the most promising. It is already an internationally traded commodity, with some 18 million tonnes traded in 2020 (about 10% of global production) (Atchison, 2021).

BOX 2.3 Three main ways to transport hydrogen by ship

Liquid hydrogen. The hydrogen molecules must be cooled to -253°C at port terminals before being loaded onto highly insulated tanker ships. As a result, the liquefaction process consumes 25–35% of the initial quantity of hydrogen. Currently, only one ocean-going ship can transport pure hydrogen, the Suiso Frontier, built by Kawasaki in late 2019 and on its first route to Australia in late 2021 (Harding, 2019).

Liquid organic hydrogen carriers (LOHCs). A slate of different organic compounds can absorb and release hydrogen through a chemical reaction. LOHCs can serve as a storage and transportation medium for hydrogen and can be transported as liquids without cooling. LOHCs are very similar to crude oil and oil products, so the existing oil transport infrastructure could even be adapted to transport LOHCs (Niermann et al., 2019).

Ammonia. Hydrogen can be turned into ammonia by reacting with nitrogen from the air, using nothing but electricity, water and air. Ammonia has a much higher energy density than hydrogen that means a larger volume of energy can be traded. There is a well-established international trade in ammonia that can be leveraged. It is currently used as a feedstock, notably to make fertilisers. It could also be used as a decarbonisation fuel, such as in the shipping industry and power generation. The downside is that ammonia is toxic if leakages occur and a potential source of nitrogen oxide emissions.

Hydrogen transport costs are still very high, but they are set to come down thanks to economies of scale, lower project risks and improvements in technology. Trade could be scaled up more rapidly in blue hydrogen than green, because it currently enjoys lower production costs and benefits from existing gas infrastructure. Green hydrogen trade is expected to increase towards 2030, thanks to improving economies of scale and the adoption of enabling policies, which will decrease production costs.

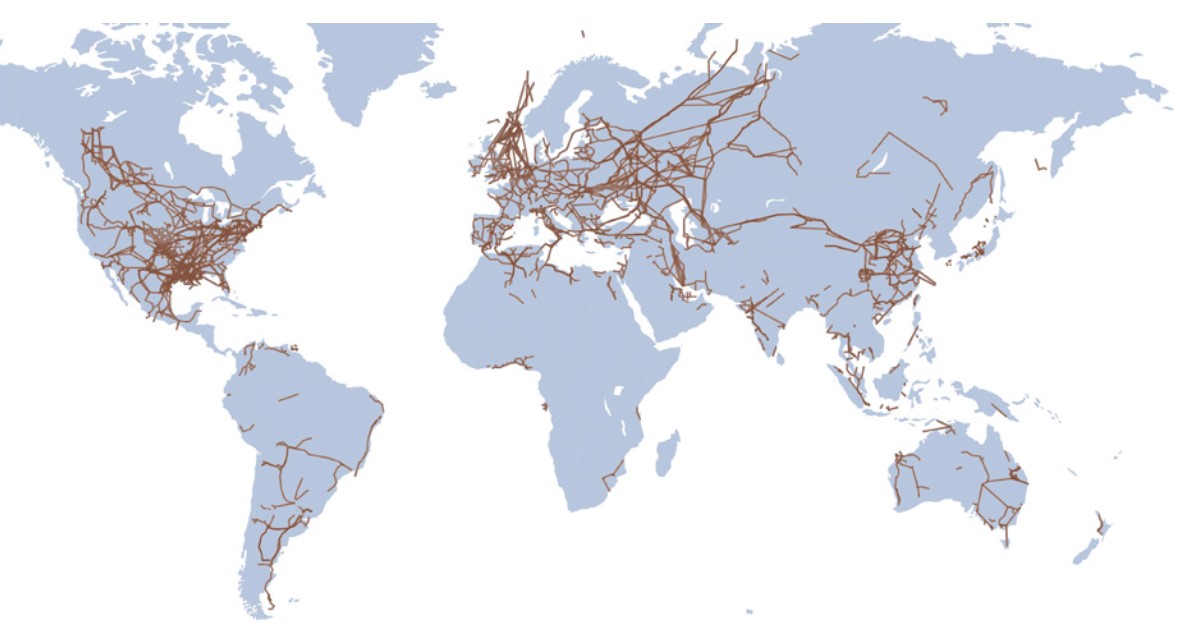

IRENA analysis suggests that about one-third of green hydrogen would be traded across borders by 2050 (IRENA, forthcoming-a). This share is slightly larger than today’s share of natural gas traded globally (24%). About half of the hydrogen trade in 2050 is likely to go through pipelines, including repurposed natural gas pipelines that exist today. The other half would be transported by long-haul ships in the form of ammonia. This situation is akin to that of natural gas, which is split into regional pipeline-based trade (48% in 2020) and global LNG trade (52%) (BP, 2021). Countries are already forging bilateral deals that could pave the way for new hydrogen trade relations (Figure 2.9).

Figure 2.9 An expanding network of hydrogen trade routes, plans and agreements

Map source: Natural Earth, 2021

Notes: Information on this fgure is based on the information contained in government documents at the time of writing.

Disclaimer: This map is provided for illustration purposes only. Boundaries and names shown on this map do not imply any endorsement or acceptance by IRENA.

Hydrogen could alter the global balance of power and bring about shifts in the relative positioning of states and regions in the international system. This chapter identifies front-runners in terms of policy, future hydrogen exporters and emerging technology leaders. It also discusses the position of fossil-fuel producer countries, which could use hydrogen to hedge against some of the transition risks as the world moves towards net zero economies. This chapter also describes how hydrogen could foster the relocation of energy-intensive industries to renewable hot spots, which could become sites of green industrialisation.

3.1 Policy front-runners and leading markets

A growing number of countries and companies are engaged in intense competition for leadership in clean hydrogen technologies. This section discusses three metrics with which to identify policy front-runners and potential leading markets: national hydrogen strategies, investments and projects on the ground.

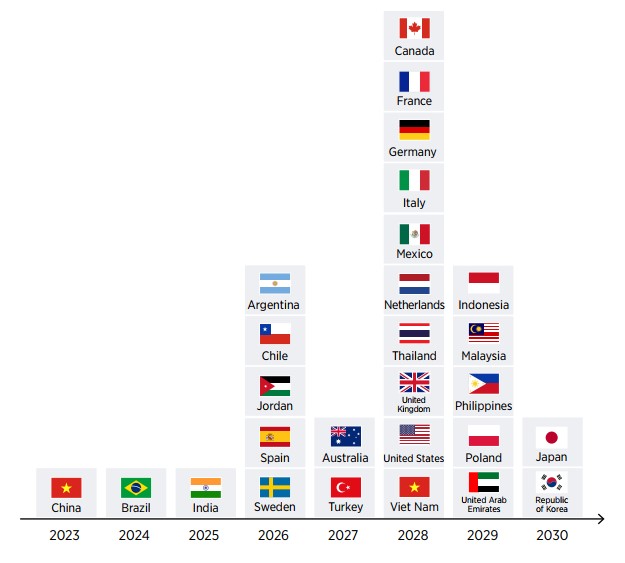

In 2017, just one country (Japan) had a national hydrogen strategy. Today, more than 30 countries have developed or are preparing hydrogen strategies (Figure 3.1), indicating growing interest in developing clean hydrogen value chains.

Figure 3.1 Hydrogen strategies and those in preparation, October 2021

Disclaimer: This map is provided for illustration purposes only. Boundaries and names shown on this map do not imply any endorsement or acceptance by IRENA.

There is considerable variation in the scope and detail of these strategies. Box 3.1 describes the vision and focus of selected countries and regions that could become early leading markets for hydrogen because of their market size and/or ambitious hydrogen plans. These large markets are well positioned to set standards and other rules of the game if their strategies and plans are operationalised.

BOX 3.1 Early adopters? Hydrogen visions in selected front-runner countries and regions

CHINA: With annual consumption of more than 24 million tonnes, China is the world’s largest user and producer of hydrogen. Production of hydrogen, which is predominantly coal-based, accounts for 3-5% of China’s coal consumption.14 Since 2019, China has had more than 30 green hydrogen projects in the works. Its first hydrogen roadmap, issued in 2016, focused on hydrogen applications in transport (Strategy Advisory Committee of the Technology Roadmap and SAE-China, 2016). With around 8 400 fuel cell electric vehicles (FCEVs) deployed, China has the world’s third-largest FCEV fleet (after the Republic of Korea and United States), and it leads the world in the deployment of fuel cell trucks and buses (IEA, 2021c). In the current Five-Year Plan (2021-2025), hydrogen is one of China’s six industries of the future (CSET, 2021). Although the country does not yet have a national strategy for hydrogen, 16 provinces and cities have launched five-year plans that feature it.

EUROPEAN UNION: The European Union (EU) issued its hydrogen strategy in July 2020. It identified hydrogen as a key priority for achieving the European Green Deal. The strategy focuses on renewable hydrogen. It includes the installation of 40 gigawatts of renewable hydrogen electrolysers in the European Union by 2030 (European Commission, 2020a). The European Union aspires to become the industrial leader in clean hydrogen. To achieve this goal, it launched the Clean Hydrogen Alliance. Some EU countries expect to become large-scale importers of hydrogen; others expect to become exporters or transit hubs.

INDIA: India launched its National Hydrogen Mission in August 2021, with the ambition of becoming “a global hub for green hydrogen production and export”. Prime Minister Narendra Modi considers green hydrogen vital to making a “quantum leap” towards achieving energy independence by 2047 (Recharge News, 2021a). The government is considering making it mandatory for refineries and fertiliser plants to use some green hydrogen. India is the world’s largest ammonia importer, a key input for fertiliser production, with imports of USD 1.27 billion in 2019 (UN Comtrade, 2021).

JAPAN: Japan was the first country to adopt a national hydrogen strategy in 2017. It aims to become the world’s first “hydrogen society”, through widespread use of hydrogen across all sectors of the economy (METI, 2017). Its plan is backed by considerable government investment in hydrogen technologies and infrastructure. In 2020, around USD 670 million was invested in the hydrogen and fuel cell business (Japan Ministry of Environment, 2020), and mobility targets were set for 800 000 FCEV units and 900 hydrogen fuelling stations by 2030 (CSIS, 2021). It is developing long-term supply agreements for hydrogen, like those that spearheaded the liquefied natural gas trade (METI, 2017).

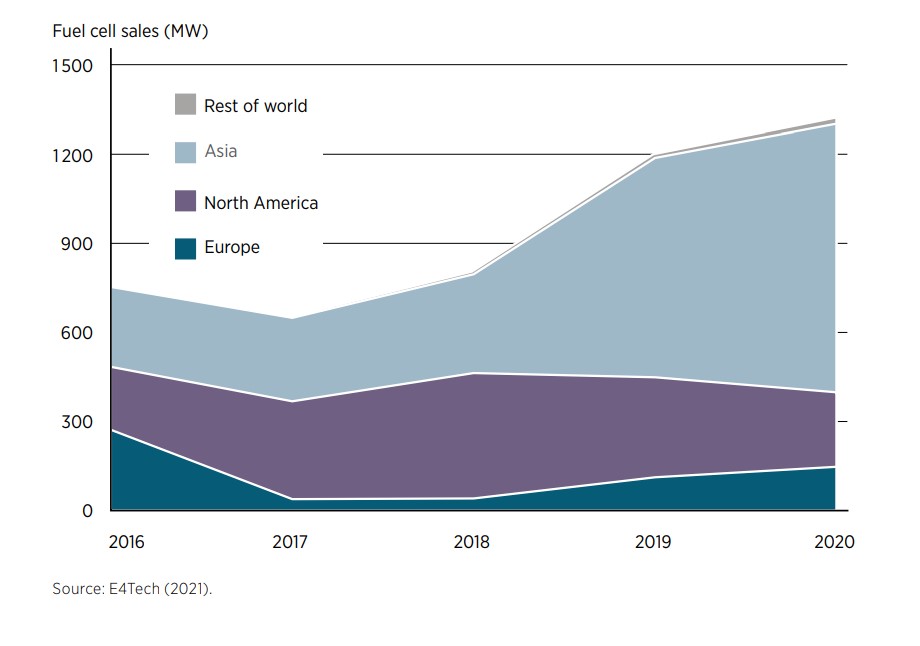

REPUBLIC OF KOREA: The Republic of Korea’s 2019 hydrogen roadmap identified hydrogen as an engine of economic growth and job creation. The country seeks to become a global leader in producing and deploying FCEVs and large-scale stationary fuel cells for power generation (CSIS, 2021). By 2020, around 10 000 passenger FCEVs had been deployed, more than in any other country (E4Tech, 2021). The government aims to increase that number to 200 000 by 2025 as part of the Green New Deal (MOEF, 2020). It also plans to use hydrogen to power 10% of the country’s cities, counties and towns by 2030 and 30% by 2040 (Korea Herald, 2019). The government expects hydrogen to become the country’s largest single energy carrier in 2050, accounting for a third of total energy consumption (Recharge News, 2021b) and is exploring hydrogen imports with various supplier countries, including Australia and Saudi Arabia.

THE UNITED STATES OF AMERICA: The United States is the second-largest consumer and producer of hydrogen in the world, accounting for 13% of global demand. Until 2020, it was the world’s largest FCEV market, led by California, which has supported the sector for almost a decade through the Clean Vehicle Rebate Program. In November 2021, the United States signed the Infrastructure Investment and Jobs Act into law. It dedicates USD 9.5 billion to accelerating the development of clean hydrogen technology. The United States also launched the Hydrogen EarthShot to bolster the development of clean hydrogen projects. It sets an ambitious "111 goal": to reduce the cost of clean hydrogen to USD 1 per 1 kilogramme in 1 decade.

The COVID-19 pandemic has heated up the race for leadership in clean hydrogen, as many countries recognise the importance of hydrogen for addressing the twin challenges of climate change and economic recovery from COVID-19. Significant shares of countries’ stimulus funds have been earmarked for hydrogen projects, bringing hydrogen into the realm of geoeconomic competition.

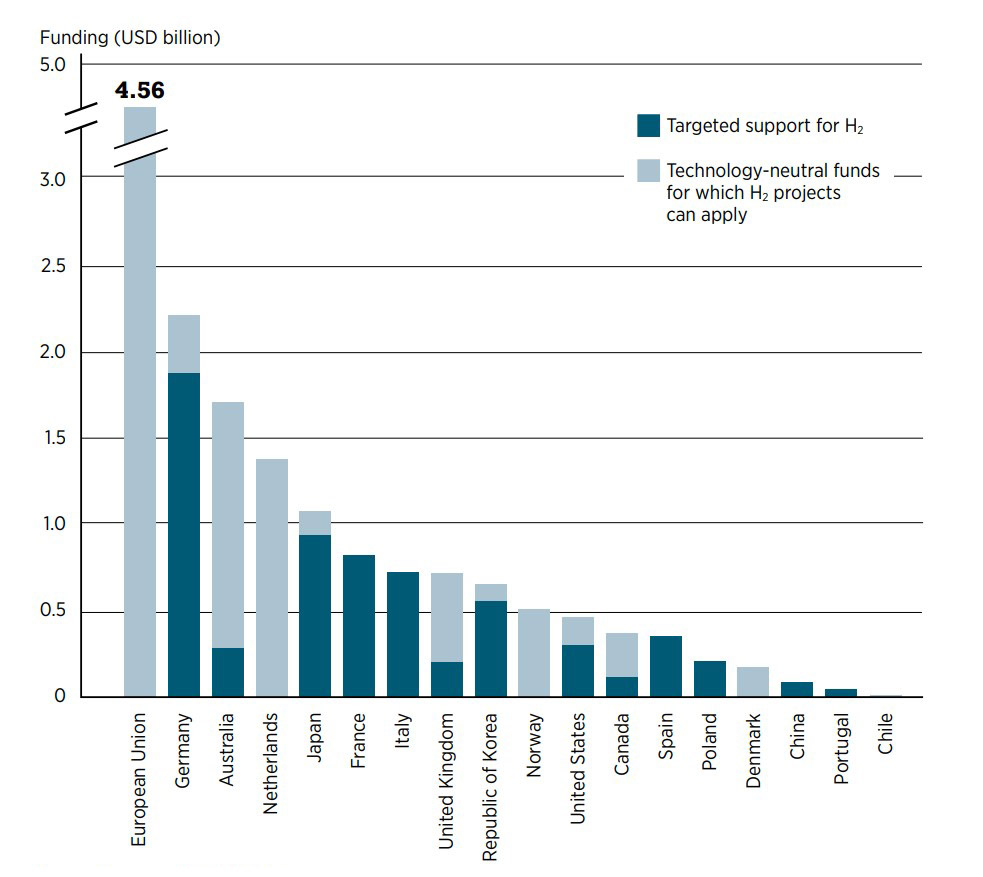

By early August 2021, governments had allocated at least USD 65 billion in targeted support for clean hydrogen over the next decade, with France, Germany and Japan making the most significant commitments (Figure 3.2). These amounts are sizeable, but they pale in comparison with energy sector subsidies, which amounted to USD 634 billion in 2017, 70% of which supported fossil fuels (IRENA 2020c).

Figure 3.2 Average annual funding potentially available for hydrogen projects, 2021-2030

Note: Figure provides a snapshot of support to hydrogen in selected countries as of 5 August 2021. It does not show support mechanisms that have been announced since or are under discussion, such as the hydrogen production tax credit proposed by the United States (US Congress, 2021).

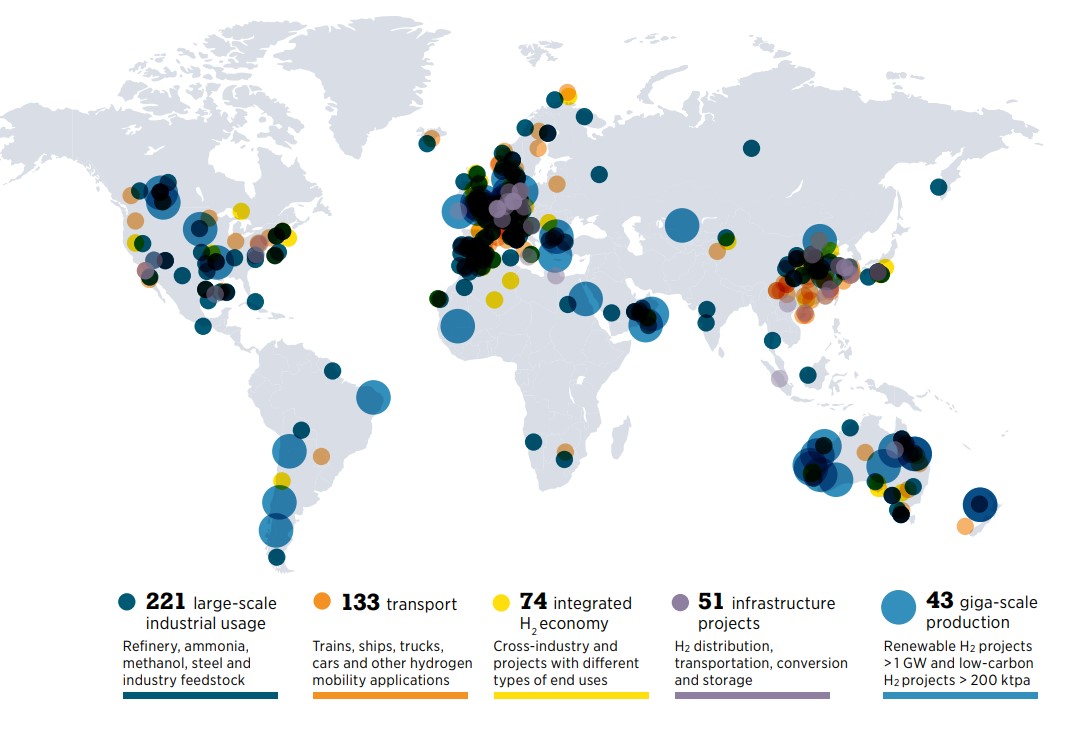

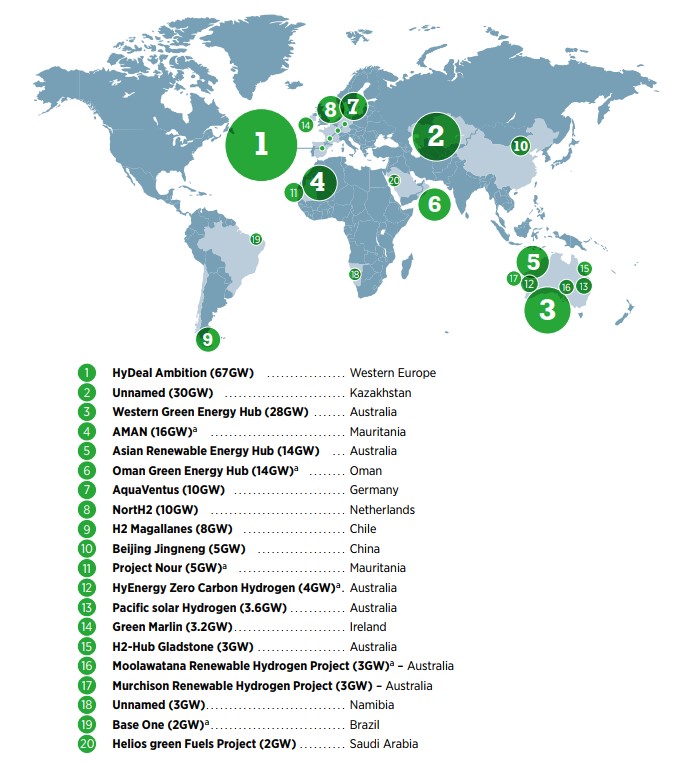

On the back of these national plans and support schemes, investment in clean hydrogen has taken off in recent years (Figure 3.3). As of November 2021, global announcements of hydrogen projects by 2030 add up to USD 160 billion of investment, with half of the investments being planned for green hydrogen production using renewable energy sources and electrolysis (Hydrogen Council, 2021).

Figure 3.3 Clean hydrogen projects and investment as of November 2021

Note: The figure describes large-scale projects only, including commissioning after 2030. It does not include more than 1 000 small-scale projects and project proposals. GW = gigawatt; H2 = hydrogen; ktpa = kilotonnes per annum.

Disclaimer: This map is provided for illustration purposes only. Boundaries shown on this map do not imply any endorsement or acceptance by IRENA.

The pipeline of announced electrolyser projects reached over 260 GW globally by October 2021, and, if implemented, would bring an additional 475 GW of wind and solar PV capacity online by 2030 (IEA 2021d).15 Although this is a dramatic increase from the 0.3 GW of electrolysis that was installed in 2020, it is far from the 160 GW that must be installed on average every year through 2050 to meet the 1.5°C goal (IRENA, 2021a).

With around half of the world’s announced megawatt-scale projects, Europe is surging ahead, driven largely by strong momentum in ambitious decarbonisation policies, national strategies and government support. Europe is followed by Asia (23% of announced projects) and North America (13%). The largest volumes of clean hydrogen are projected to come from Europe and Oceania, which together account for more than half the capacity through 2030, most of which is from renewables. Giga-scale projects have also been announced that focus on hydrogen exports in Africa, Latin America, the Middle East and Oceania (Box 3.2).

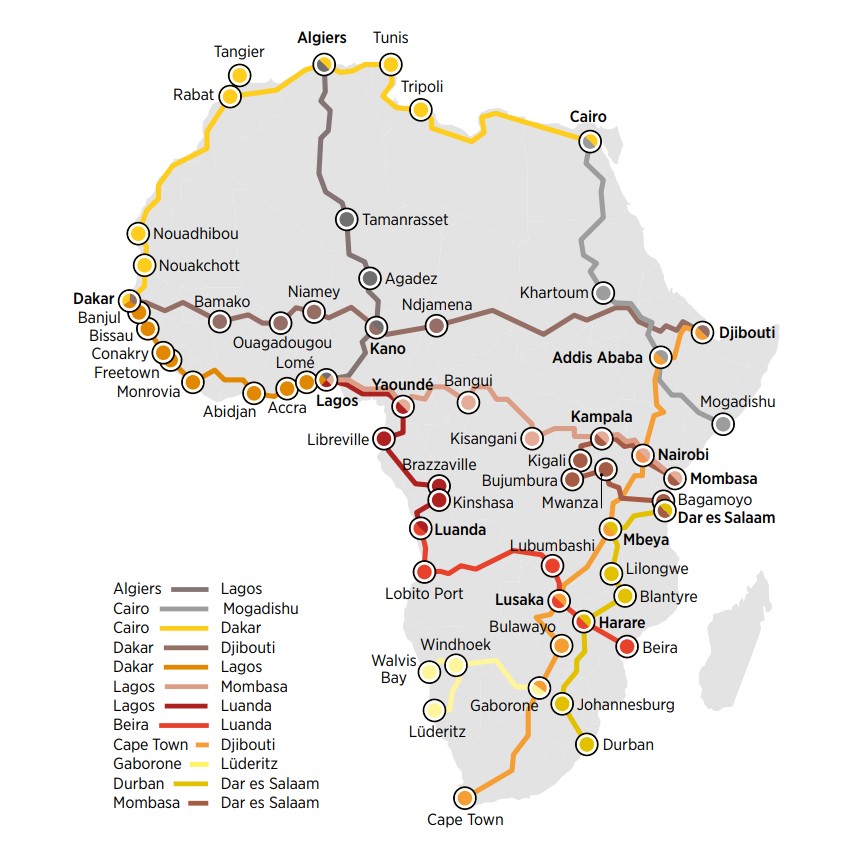

BOX 3.2 Hydrogen projects in Africa

Africa’s vast renewable potential, along with its experience with the previous generation of electrolyser from the early 20th century, has drawn the attention of international investors that have announced several green hydrogen projects.

EGYPT and ZIMBABWE already have installed over 100 megawatts (MW) of electrolysers. In December 2021, Egypt announced a new 100 MW project for producing green ammonia.

In May 2021, CWP Global, a renewable development company, signed a memorandum of understanding with the Government of MAURITANIA to develop a 16 gigawatt (GW) electrolysis project, in tandem with 45 GW of renewables. The total cost of the project is expected to be USD 40 billion (Energy Voice, 2021). Mauritania also gave exclusive development rights to Chariot (an oil and gas company active in Brazil, Morocco, and Namibia) to develop up to 10 GW of offshore and onshore wind for green hydrogen production, a project that could spearhead Africa’s first offshore wind farm (Recharge News, 2021c).

At COP26, the Government of NAMIBIA announced the selection of HYPHEN Hydrogen Energy as the preferred bidder for a green hydrogen project. The first phase of the project would bring 2 GW of renewable-electricity generation capacity, along with the electrolyser capacity to produce green hydrogen for conversion into ammonia. Further expansion phases in the late 2020s would raise the total investment value to USD 9.4 billion, which is almost in line with Namibia’s current GDP. Once complete, the integrated facility would have a renewable generation capacity of 5 GW and an electrolyser capacity of 3 GW, with surplus electricity capacity to be fed into the Namibian grid and potentially into the regional power pool. The project will use desalinated water, part of which will be supplied to communities in nearby Luderitz (Engineering News, 2021).

3.2 A new class of energy exporters

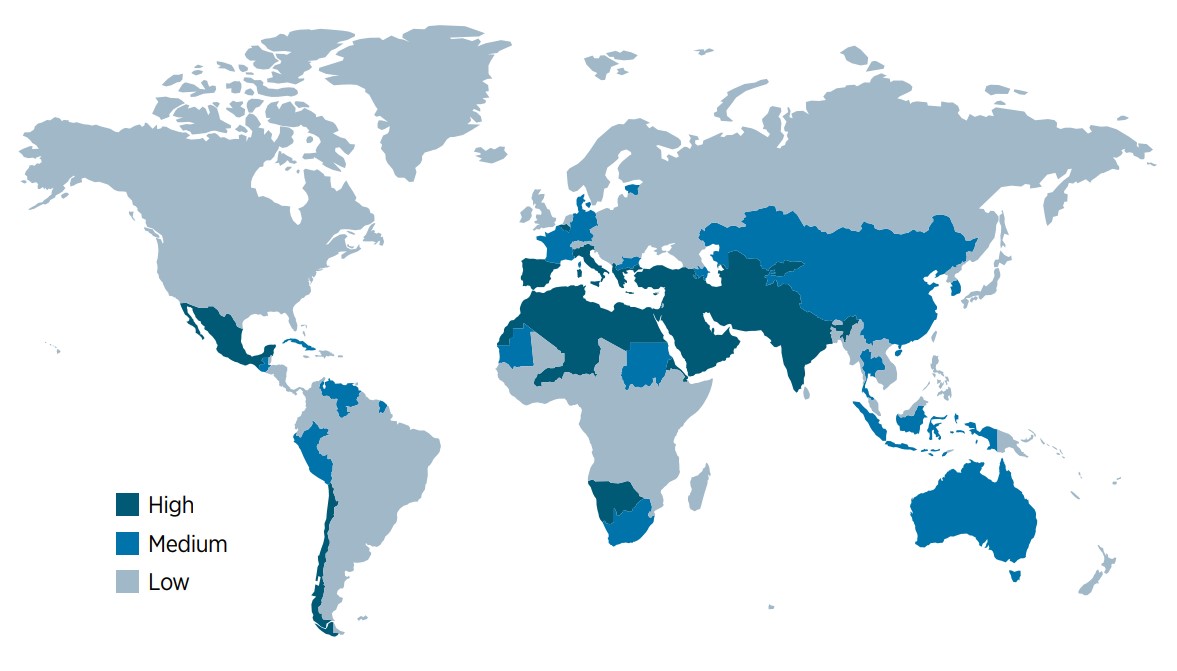

Countries and regions with high renewable potential and a low levelised cost of electricity can use their resources to become major producers of green hydrogen. The ability of different regions to produce large volumes of low-cost green hydrogen varies widely. Africa, the Americas, the Middle East and Oceania are the regions with the highest technical potential; Europe, Northeast Asia and Southeast Asia have fewer resources for producing green hydrogen (Figure 3.4). Countries’ technical renewable potential is not the only factor determining how likely they are to become major producers of green hydrogen. Many other factors come into play, including existing infrastructure and “soft factors” (e.g. government support, business friendliness, political stability) and the current energy mix and industry (e.g. renewable plans, potential demand for hydrogen).

One way to foresee future importers and exporters of green hydrogen is to compare their domestic production potential with their expected hydrogen demand by 2050, and the cost of import.16 Three groups of countries can be identified. The first group includes countries with low cost green hydrogen production that could develop into exporters. They can leverage their renewable markets to attract investments in green hydrogen production. Australia, Chile, Morocco and Spain are among such net hydrogen exporters. The second group includes countries that can become self-sufficient in green hydrogen. These countries have sufficient production potential to cater to their own needs without resorting to imports. It includes China and the United States. The third group includes countries that will need imports to satisfy domestic demand, including Japan, Republic of Korea, and parts of Europe and Latin America.

Of course, this picture can significantly change with investment at scale to develop new renewable markets and hydrogen infrastructure where potentials are abundant but lacking access to technology, know-how and local capabilities.

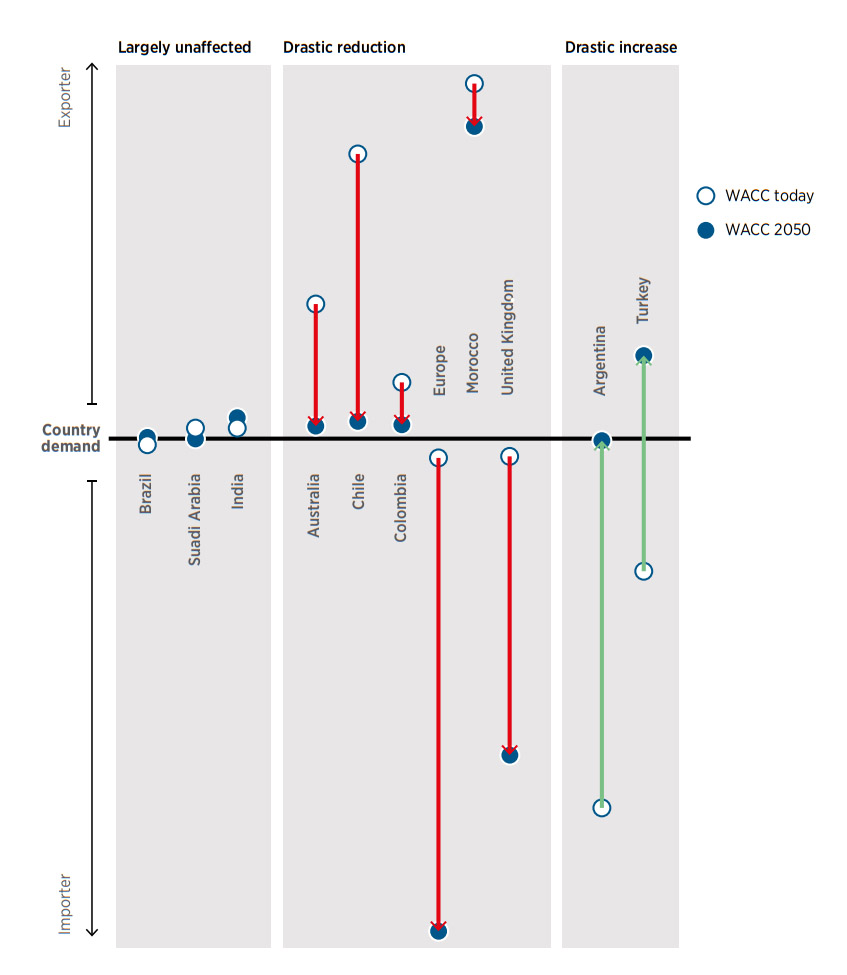

One of the key unknowns is the cost of capital (weighted average cost of capital or WACC), which is currently differing greatly between countries (Box 3.3).

BOX 3.3 The importance of capital cost assumptions for hydrogen trade projections

In a future dominated by renewables, energy cost will be dominated by the capital cost. It is often seen as a prudent approach to assume that the cost of capital differences seen around the world today will persist in 2050 (Egli, Steffen and Schmidt, 2019). However, if one assumes that these differences even out (Bogdanov, 2019), the picture changes completely (Figure 3.5). Latin America, the Middle East and Turkey would become green hydrogen exporters instead of importers, while Spain would move in the opposite direction. The export potential of countries such as Australia and Chile, which already enjoy low WACC today, would be severely diminished, while the import needs of the EU and Germany would rise significantly.

Figure 3.5 Impact of cost assumptions on hydrogen production of selected countries

Experts believe that Australia, Chile, Morocco, Saudi Arabia and the United States are best placed to emerge as major clean hydrogen producers by 2050 (see Figure B.3 in Annex). Some of these countries, namely Australia, Saudi Arabia and the United States, are current energy exporters. They can retain their role as energy exporters, although they will enter a much more competitive market, as green hydrogen can be produced almost anywhere. Other countries, such as Chile, Morocco and Namibia, are currently net energy importers.17 For these countries, a green hydrogen transformation represents a complete reversal of fortune, as ample renewable potential opens new possibilities. Countries that succeed in becoming major exporters of green hydrogen and derived fuels also stand to gain in geostrategic importance (Box 3.4).

BOX 3.4 From energy importer to exporter? Hydrogen activities in selected fossil-fuel importing countries with green hydrogen export potential

CHILE: Chile launched a green hydrogen strategy in 2020. It aims to reach 5 GW of electrolyser capacity by 2025 and 25 GW by 2030, produce the world’s cheapest hydrogen by 2030 and become one of the world’s top three hydrogen fuel exporters by 2040 (Gobierno de Chile, 2020). It is estimated that the country could be exporting USD 30 billion worth of green hydrogen and derivatives by 2030 (Mander, 2020). Hydrogen has attracted growing attention in Latin America, mostly because of the region’s high renewables potential. Several countries in the region have either published or are preparing national hydrogen strategies and roadmaps (Figure 3.1).

MOROCCO: Morocco created a National Hydrogen Commission in 2019 and published a green hydrogen roadmap in January 2021. Hydrogen is mentioned as a key growth sector in the national economy. By 2030, the country envisages a local hydrogen market of 4 terawatt hours (TWh) and an export market of 10 TWh, which, taken together, would require the construction of 6 GW of new renewable capacity and support the creation of more than 15 000 direct and indirect jobs (MEM, 2021).

NAMIBIA: The country’s vast solar and wind energy resources have attracted attention from investors. The government identified green hydrogen and green ammonia as emerging export opportunities (Government of Namibia, 2021). It set up a national Green Hydrogen Council and appointed a special green hydrogen commissioner. The government is also looking into setting up a blade manufacturing plant for wind turbines, a green steel plant and an ammonia fertiliser production line (Weidlich, 2021). The size of these proposed projects is very large relative to Namibia’s economy, pointing to the transformative potential of green hydrogen for the national economy (Geingob, 2021).

3.3 Transition pathway for fossil fuel producers

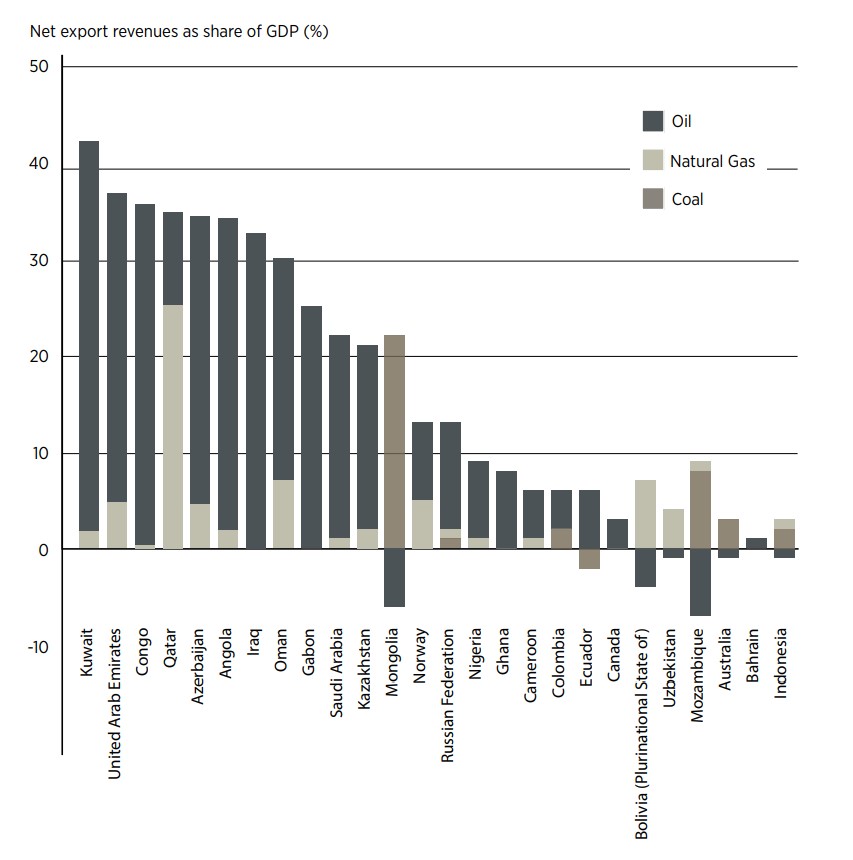

The energy transition will significantly affect fossil fuel producers: It is highly likely that large parts of oil, gas and coal reserves will never be extracted and monetised. A foreshadowing of these effects was evident during the COVID-19 pandemic in 2020, when lower prices and collapsing demand wiped out around a quarter of the value of all oil and gas reserves (IEA, 2020). Although low-cost producers may see an increase in their market share as the energy transition progresses, even they would see large declines in revenues as the overall market is expected to shrink (IEA, 2021a). Several oil and gas producers have already seen their sovereign credit ratings downgraded. The 20 countries with the highest net fossil fuel exports to Gross domestic product (GDP) ratio (Figure 3.6) suffered a median net downgrade of 1.6 notches in their credit ratings between 2015 and 2020 (Fitchratings, 2021). As decarbonisation progresses, producer countries will have to move their economies away from a reliance on oil and gas.

Figure 3.6 Stranded asset risk for major net fossil fuel exporters, 2019

Note: The price of Brent crude oil (the international benchmark) averaged USD 64 per barrel in 2019. Its average in 2010-2020 was USD 76.2 per barrel (EIA, n.d.).

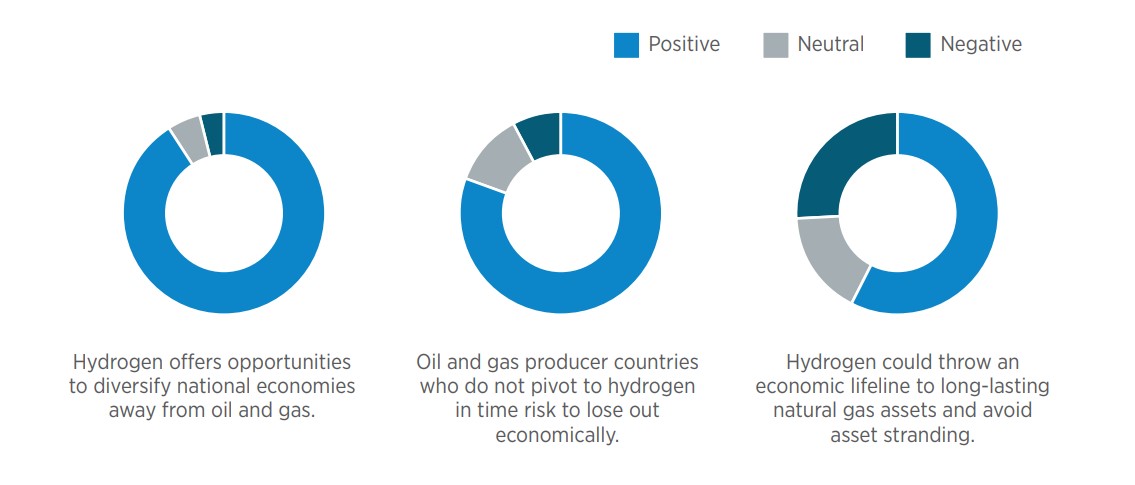

Clean hydrogen offers an attractive transition pathway for oil- and gas-exporting countries to diversify their economies as major export markets move towards low- and zero-carbon fuels and energy carriers (Figure 3.7). Oil- and gas-producing countries are well placed to pivot to hydrogen, as they can leverage established energy export infrastructure (ports, pipelines and storage facilities); a skilled workforce familiar with producing, converting and handling energy fuels and gases; and existing energy trade relations.

In the run-up to COP26, several exporters adopted a net zero goal, including Australia, Russia, Saudi Arabia and the United Arab Emirates. Clean hydrogen is a vital avenue for achieving these goals. Some fossil-fuel producing countries have already adopted national hydrogen strategies (e.g. Australia, Canada, Colombia, Norway, Russia and the United Kingdom) or are preparing to do so.

The strategies of fossil fuel exporters often mention the opportunity that hydrogen offers to develop new export industries (Box 3.5). Several espouse a “technology-neutral” approach and explicitly include the possibility of blue hydrogen (this is the case for Australia, Canada and Norway, for instance). Australia and Canada provide details of expected or necessary carbon capture rates for hydrogen produced from fossil fuels to be considered “clean”, which they set at or over 90% (Longden et al., 2022).

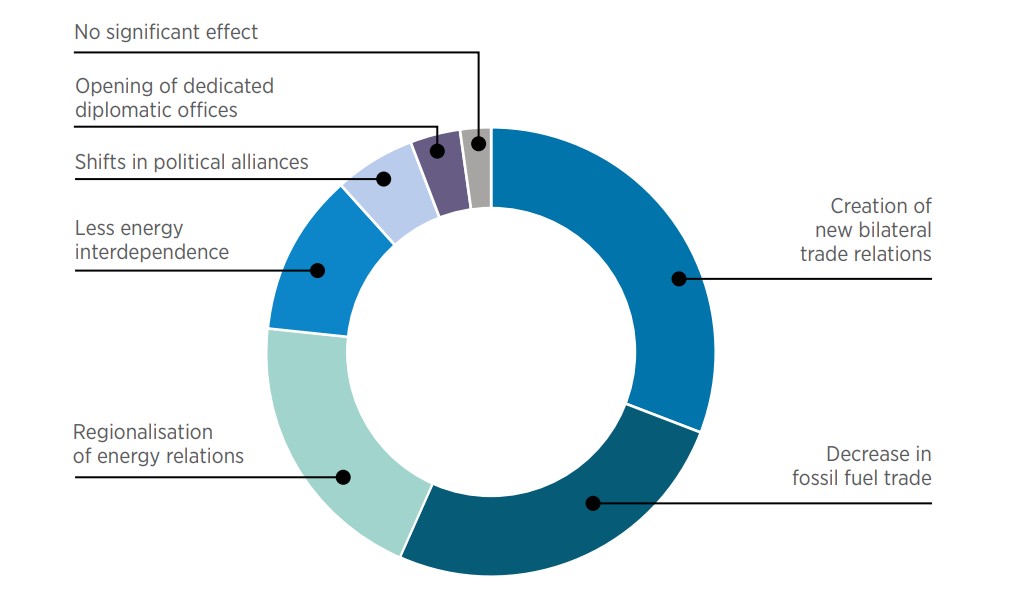

Figure 3.7 Expert views on hydrogen strategies and impacts for oil and gas producers

BOX 3.5 Pivoting to hydrogen? Hydrogen strategies of selected fossil-fuel exporting countries

AUSTRALIA: Australia aims to become a “major global player” in clean hydrogen production and trade by 2030; it considers hydrogen its “next big export”. By 2030, the country wants to be among the world’s top three exporters of hydrogen to Asian markets (Government of Australia, 2019). The government has invested over USD 1 billion to stimulate the domestic hydrogen industry, including co-sponsoring seven hydrogen hubs (Government of Australia, 2021). Nine gigawatt-scale green hydrogen projects are planned or under development, although the government does not rule out blue hydrogen production. Australia has also forged deals with prospective export markets, such as Germany, Japan, and Singapore.

CANADA: Canada’s strategy identifies new export opportunities and states that the country is well placed to become “a leading global clean fuels exporter” (Government of Canada, 2020). By 2050, it aims to be one of the world’s top three clean hydrogen producers. Although Canada is open to many production pathways, its strategy mentions the need to ultimately transition to an increasing percentage of renewable or zero-emission production methods and refers specifically to the country’s large hydropower capacity.

NORWAY: Norway is a major gas exporter to Europe, delivering around a quarter of Europe’s gas needs, mostly through pipelines. Equinor, a Norwegian energy company, is currently studying the possibility of delivering natural gas to Germany or the Netherlands, where it can be converted into blue hydrogen. The hydrogen would then go to a steel mill in Duisburg, Germany, and the carbon dioxide would be shipped back for storage under the seabed of the Norwegian shelf of the North Sea (Equinor and OGE, 2019).

OMAN: Oman is preparing a national hydrogen strategy with the aim of establishing a hydrogencentric society by 2040. It also plans to become a large-scale exporter of green hydrogen or green ammonia. Several gigawatt-scale projects have already been announced, all capitalising on the abundant solar and wind resources in the al Wusta governorate and eyeing the Arabian sea port of Duqm for exports. The biggest of these projects will be powered by 25 GW of solar and wind (Argus, 2021).

RUSSIA: Russia aims to become one of the world’s largest exporters of clean hydrogen, mainly the blue variant. In the words of Prime Minister Mikhail Mishustin, “hydrogen energy will reduce the risks of losing energy markets” (The Russian Government, 2021). By 2030, Russia aims to account for 20% of the global hydrogen market, which is larger than its current share of the natural gas market (RIA Novosti, 2021). By the middle of the century, Russia foresees exporting up to 50 million tonnes of hydrogen, bringing an additional USD 23-100 billion to the annual budget (Patonia, 2021).

SAUDI ARABIA: In July 2020, the Helios Green Fuel Project was announced, a USD 5 billion green hydrogen and green ammonia plant powered entirely by solar and wind. The plant is expected to start operation in 2025 in the planned megacity of Neom, on the shores of the Red Sea near Saudi Arabia’s borders with Egypt and Jordan (HELIOS, n.d.). Saudi Aramco, the national oil company, acquired a 70% stake in the Saudi Basic Industries Corporation, the world’s third-largest exporter of ammonia (Aramco, 2020a). Saudi Aramco made the first shipment of blue ammonia to Japan in September 2020, for use in power generation (Aramco, 2020b). Saudi Energy Minister Prince Abdulaziz bin Salman said at a press briefing in late 2020 that his country “will not be challenged in its record of being the biggest exporter of hydrogen on earth” (Ratcliffe, El Wardany and Martin, 2020).

UNITED ARAB EMIRATES (UAE): UAE’s hydrogen roadmap, released in November 2021, aims to establish the country as a leader in blue and green hydrogen exports. The ambition is to capture 25% of the global low-carbon hydrogen market by 2030. More than seven projects are already in the works via main stakeholders, including the Abu Dhabi Hydrogen Alliance, which is made up of the Abu Dhabi National Oil Company (ADNOC), the Abu Dhabi state investor Mubadala and the state-owned holding company ADQ. ADNOC has concluded partnerships with countries such as Japan (ADNOC, 2021a), Malaysia (ADNOC, 2021b) and the Republic of Korea (ADNOC, 2021c) to explore options for hydrogen trade, and it has already sold four test cargoes of blue ammonia (Emirates News Agency, 2021).

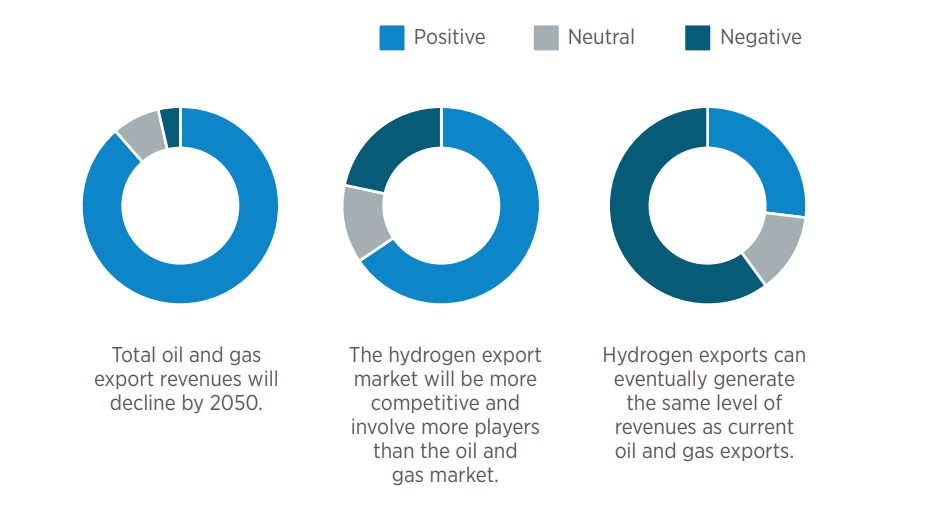

The blue hydrogen production route might appeal to countries with cheap gas reserves. Several oil and gas exporters – including Australia and some of the sunny and windy countries of North Africa and the Persian Gulf – could also become competitive green hydrogen producers. Total oil and gas export revenues are expected to fall significantly by 2050. Although cross-border hydrogen trade might grow significantly, experts doubt that hydrogen will generate as much revenues as oil and gas do today (Figure 3.8). Hydrogen can thus not be considered a new, zero-carbon version of oil. Unlike oil and gas, hydrogen is a conversion business, not an extraction business, which will likely limit the possibilities to capture economic rent (UCL, n.d.). The hydrogen business will be more competitive and involve more players than oil and gas. As the costs of green hydrogen fall, new and diverse participants will enter hydrogen markets.

Figure 3.8 Expert views on future hydrogen revenues and market structure

3.4 Rise of new technology leaders

Over the past few years, zero-carbon solutions have grown more rapidly than expected, giving way to new sources of wealth creation and destruction (Systemiq, 2020). Having a stake in the value chains of climate-safe energy technologies, such as clean hydrogen, can boost a country’s economic competitiveness, national security and energy independence.

Technology leadership might be developed around many aspects of the hydrogen value chain. Among countries that aspire to export hydrogen or derivatives, there is wide variation in technology ownership, which may affect their ability to influence standards and operating frameworks. Australia, Canada and Saudi Arabia, for example, developed hundreds of inventions between 2010 and 2020 (IRENA INSPIRE webtool, 2021). Colombia, Egypt, Morocco, Oman and the United Arab Emirates saw much less activity (with three or fewer hydrogen-related patents filed by each of these countries in this period). In each of the segments of the value chain, countries could play leading roles in multiple ways (see Figure B.8 in Annex). This section focuses on innovation and manufacturing.

Figure 3.9 Technology leadership opportunities in green hydrogen value chains

Note: CO2 = carbon dioxide; N2 = dinitrogen.

Innovation leaders

The landscape of hydrogen technologies and companies is still in flux; renewed policy focus has triggered innovation along the hydrogen value chain. To assess how countries are positioned in the clean hydrogen innovation race, it is useful to look at two metrics: research and development (R&D) spending and patents.

The countries of the Organisation for Economic Co-operation and Development (OECD) have historically accounted for the bulk of global R&D spending in hydrogen, although China is quickly catching up, as evidenced by the government’s six-fold increase in hydrogen R&D expenditure in 2019 (IEA, 2021c). Public funding for hydrogen has been split relatively equally between fuel cells and other applications (IEA, 2021c). If the recent growth in hydrogen R&D is sustained, government support could return to levels not seen since the late 2000s.

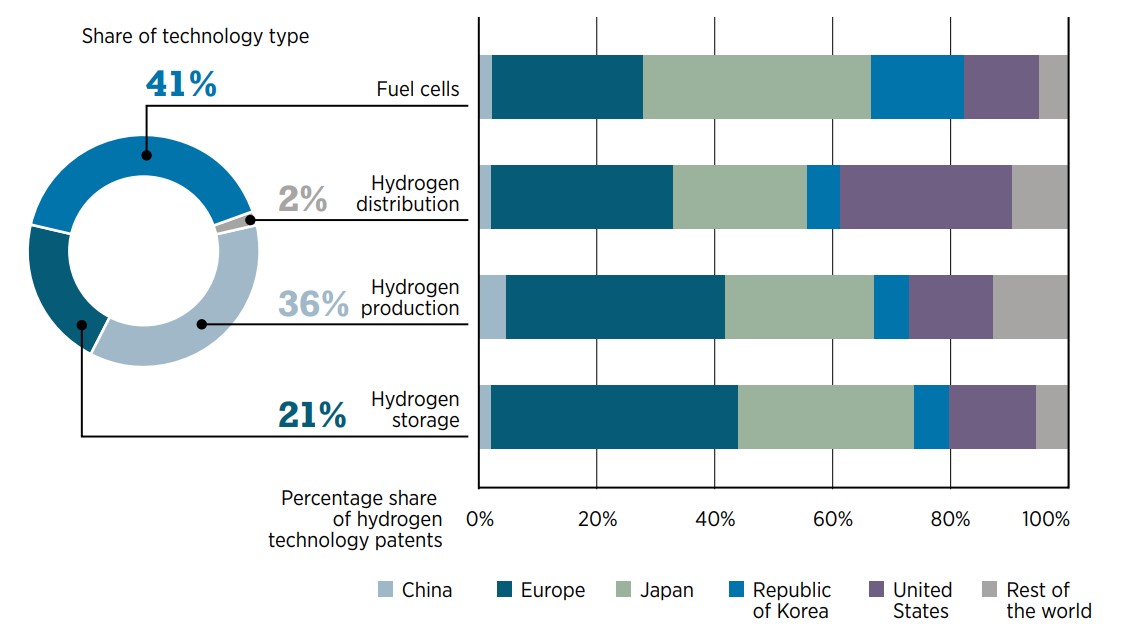

The OECD countries account for the vast majority of patents in the field of hydrogen. Japan dominates fuel cell research, holding almost 40% of all patents; Europe leads in hydrogen production (primarily electrolysers) and hydrogen storage technologies (Figure 3.10). Fuel cells account for about 41% of all hydrogen-related patents, but the fastest growth in recent years has been recorded in other areas, such as production and storage. Benefits, such as domestic value added, will depend on where the intellectual property is concentrated.

Figure 3.10 Geographic distribution of hydrogen-related patent families, 2010-2020

Note: Patent data for 2020 are not complete, because of confidentiality in the early stage of the patenting process. Analysis focuses on the top five players and their patent offices. Patent applications filed at the World Intellectual Property Organization are allocated to the corresponding receiving office. Equal shares are assigned to applicants and patent offices in the patent family. Hydrogen technology is defined based on the subcategory patent codes of the Cooperative Patent Classification that concern the development of enabling technologies for the reduction of greenhouse gas emissions related to energy generation, transmission or distribution – insofar as hydrogen is specifically mentioned (Y02E60/34 Distribution, Y02E60/50 Fuel Cells, Y02E60/36 Production and Y02E60/32 Storage).

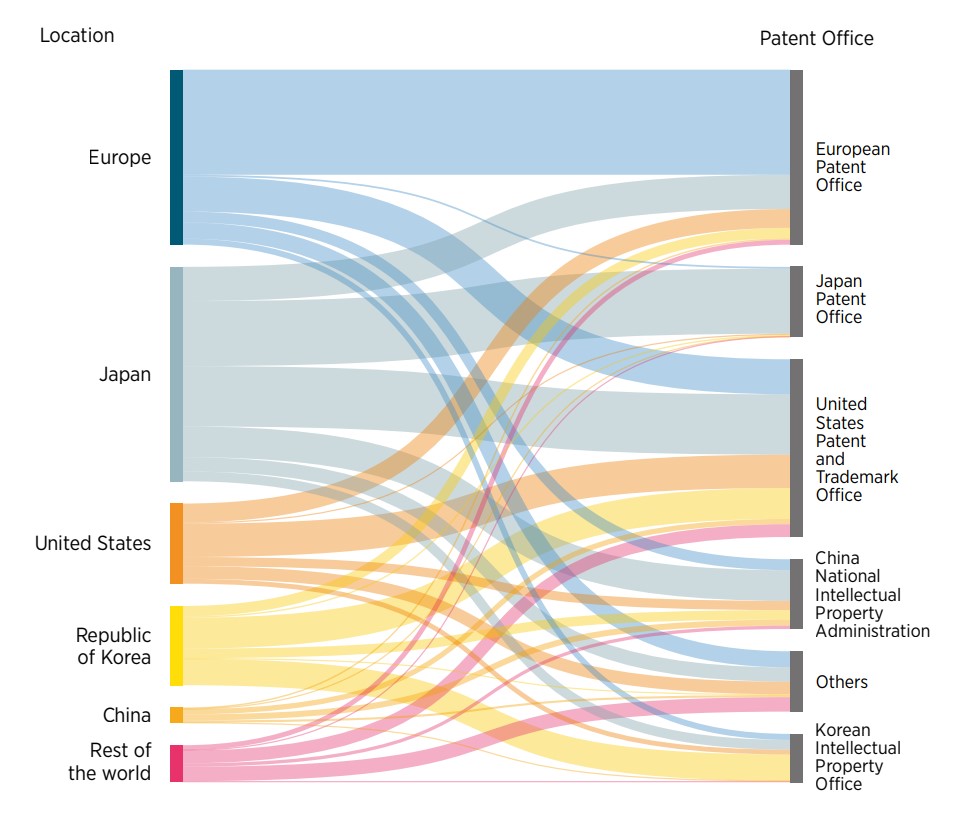

Looking at regions where hydrogen-related inventions are protected can give a sense of where technology leaders are looking at commercialisation (Figure 3.11). In 2010-2020, Europe and the United States were the two geographical areas where inventions were highly protected. Most of European inventions (60%) are protected in the European market; the rest are protected in other areas, particularly the United States, where European inventions make up about 20% of all patents. Although Japan developed the largest number of inventions (36% of the total), very few are protected in Japan from abroad, indicating high technology capability but fewer market opportunities. The growing number of international technology partnerships could see Japan emerge as a technology leader, even as a net importer of hydrogen.

China lies at the opposite end of the spectrum: more than 90% of inventions protected by the China National Intellectual Property Administration come from abroad. In the past decade, China has remained an attractive market as a manufacturing hub, a trend that could continue.

Figure 3.11 Flow of inventions in hydrogen technology, 2010-2020

Note: Flow of inventions from country developing hydrogen-related technologies (on the left) to the market where these are protected (on the right side).

More information available at: https://public.tableau.com/app/profile/irena.resource/viz/IRENA_INSPIRE_Hydrogen_Patents/HydrogenTech

Equipment manufacturing

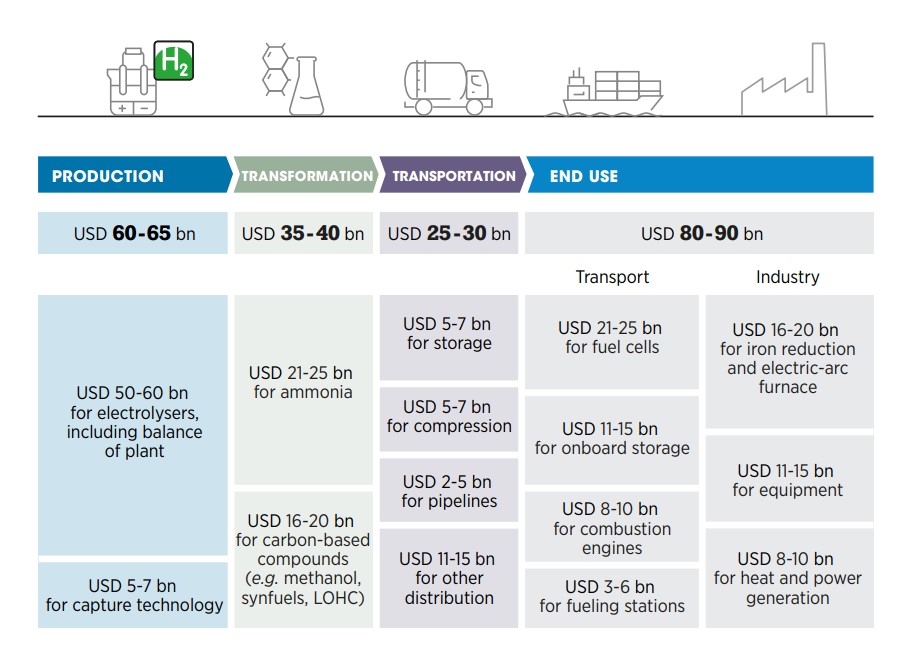

The nascent market for hydrogen-related equipment is highly complex and fragmented. A full discussion of all technologies involved is beyond the scope of this report. This section focuses on the two key hardware pieces in the hydrogen value chain: electrolysers and fuel cells. These two pieces of equipment offer the greatest opportunities for countries and companies to capture value in the coming years and decades and establish themselves as industry leaders. Estimates point to a USD 50-60 billion market potential for electrolysers and a USD 21-25 billion opportunity for fuel cells by the middle of the century (Figure 3.12). These technologies are more mature than technologies in other parts of the value chain. No other aspect of the hydrogen value chain was considered as strategic as electrolysers in IRENA’s expert survey, while fuel cells were deemed essential for technological leadership (see Annex).

Figure 3.12 Estimated market potential for hydrogen equipment and components, 2050

Note: LOHC = Liquid organic hydrogen carrier.

Electrolysers