The International Renewable Energy Agency (IRENA) has called for an acceleration in the pace and scale of renewable energy deployment, highlighting the importance of renewable energy not only as an effective means of reducing emissions and enhancing energy security but also as a driver of economic growth and job creation.

The proliferation of renewable energy in the power sector has so far been the most prominent deployment, but the decarbonisation of hard-to-abate sectors using renewable energy also needs attention. This digital toolkit provides actionable recommendations that decision makers can follow to accelerate global efforts to decarbonise six hard-to-abate sectors and outlines the technological pathways for short-term actions and longer-term efforts. The toolkit also maps several enablers, within key enabling dimensions, that can be used to achieve decarbonisation in these hard-to-abate sectors and presents a non-exhaustive summary of the progress and challenges of each enabler.

For some sectors, such as passenger road transport, the path to net-zero emissions is clear, as evidenced by the exponential rise in electric vehicle sales. The pace of transformation in some other sectors, however, is much slower. Some industrial and transport subsectors are substantial greenhouse gas emitters and are harder to decarbonise due to their physical, technological or market particularities.

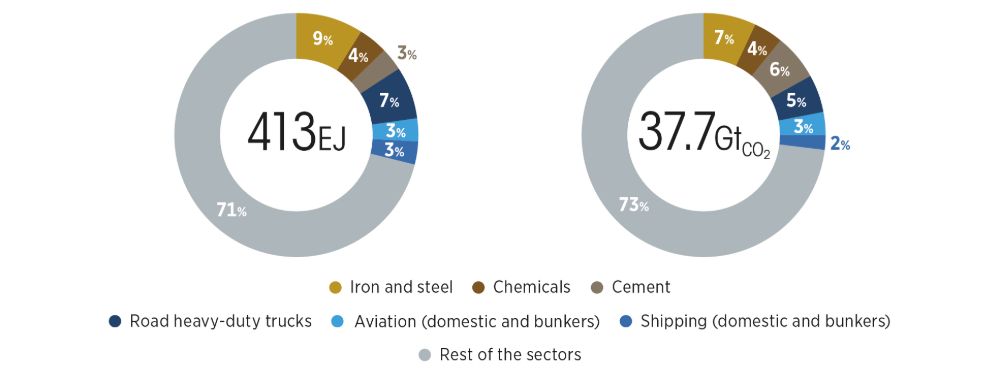

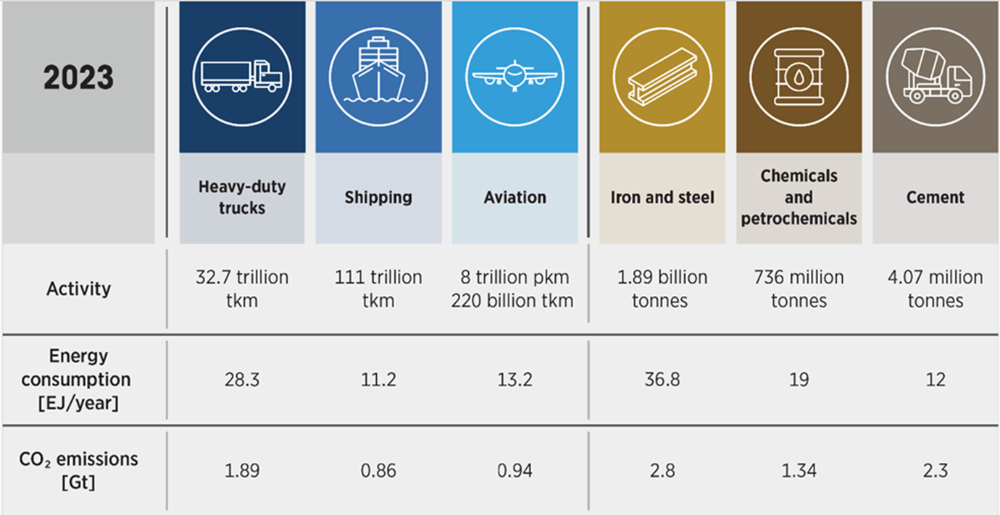

This toolkit focuses on six hard-to-abate sectors: heavy-duty trucks, shipping, aviation, iron and steel, chemicals and petrochemicals, and cement. These six sectors account for roughly 29% of the world’s energy consumption and are responsible for around 27% of total carbon dioxide (CO2) emissions (Figure ES1).

Figure ES1: Global energy consumption (top left), CO2 emissions (top right) and activity metrics (bottom) for select hard-to-abate sectors, 2023

Source: ICAO, 2023a; IEA, 2023a, 2023b; UNCTAD, 2022.

Renewables can play a central role in the decarbonisation of all hard-to-abate sectors. The drastic cost reductions observed in recent years make renewable power the cheapest source of carbon-neutral energy worldwide. There is potential for further cost reductions through technological learning and economies of scale.

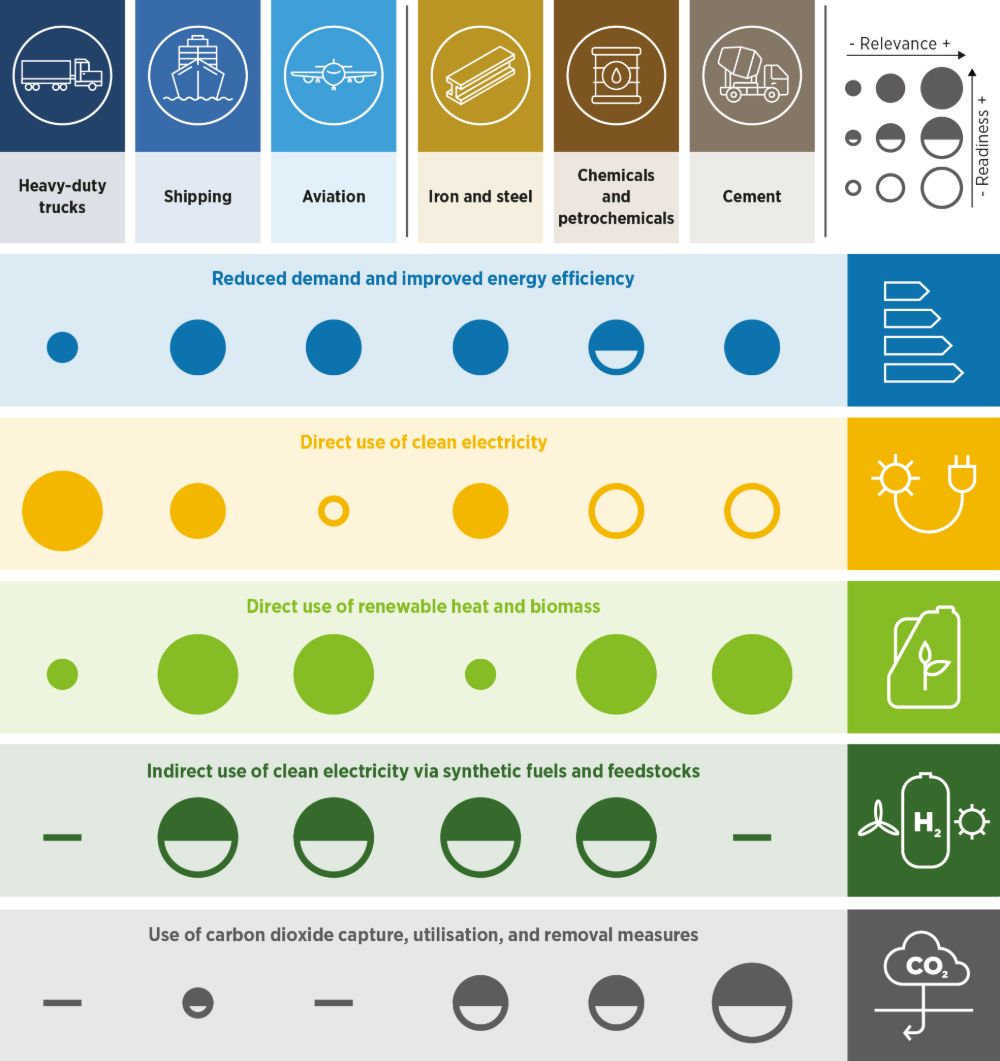

The full decarbonisation of the hard-to-abate sectors will require a combination of approaches, specific to the characteristics of each sector. However, most emission reductions will have to be achieved through a combination of five main pathways, which rely primarily on renewable energy and energy efficiency, as described in Figure ES2.

Figure ES2: Summary of key technological pathways for decarbonisation and their readiness in hard-to-abate sectors

The transition in hard-to-abate sectors requires fundamental shifts, rather than gradual steps. The window of opportunity for action to counter the global climate threat is closing fast. Solutions that deliver only partial emission reductions, such as replacing oil or coal with natural gas, will not be sufficient and will increase the risk of assets becoming stranded. Decision makers should prioritise solutions that are consistent with net-zero emissions and avoid delaying their decarbonisation objectives. Most of these solutions rely on renewable energy.

Direct electrification will play an increasing role, with important contributions in multiple applications. Some of these solutions have already reached, or close to, technological maturity. Such solutions include the use of electric arc furnaces for steelmaking, which will become more important as the share of recycled steel increases in the coming decades; battery electric trucks, which are at a technological inflection point and becoming increasingly available; heat pumps for low to medium temperature heating in industry; and cold ironing at ports. Some other applications of direct electrification, while having great potential, still need further development. These applications include electric crackers to produce primary chemicals, electrolysis of iron ores, and electric or hybrid aircraft and ships for short distances.

Bioenergy and synthetic fuels will play a critical, complementary role to electrification. Scaling up sustainable, low-carbon bioenergy solutions is not only key to the decarbonisation of shipping and aviation; it is also critical to the provision of feedstocks for chemicals and as a potential carbon source for synthetic fuels. Indirect electrification – via the production of renewable hydrogen – is also set to play an important role in achieving deep emission reductions in these sectors. Renewable hydrogen can do this as a reductant in the production of iron in primary steel production, as a form of synthetic fuel for shipping and aviation, and as a feedstock in chemical industries.

These pathways will have to be complemented by continual energy efficiency improvements, the application of the principles of the circular economy, and behavioural and process changes that reduce demand. Emissions can be further reduced through the application of CO2 capture, utilisation and/or removal measures, provided that these technologies achieve the necessary improvements in performance and economics to make them technically scalable and economically viable.

Although the technology associated with these pathways is increasingly available, in the absence of sufficiently high and widespread carbon pricing, a timely transition to renewables in hard-to-abate sectors will almost certainly require paying a premium over the cost of fossil-based systems. Cost differentials differ widely by sector and application. Despite promising progress and increased attention from policy makers, none of the hard-to-abate sectors is on a trajectory compatible with reaching net-zero emissions by mid-century.

Several enabling conditions need to be put in place to accelerate the decarbonisation of hard-to-abate sectors. This will require decisive action by governments, as well as by the private sector. The enabling conditions also have fundamental implications in terms of national and international policy and regulatory environments, technology and infrastructure planning, global commodity markets, and international supply chains and business models.

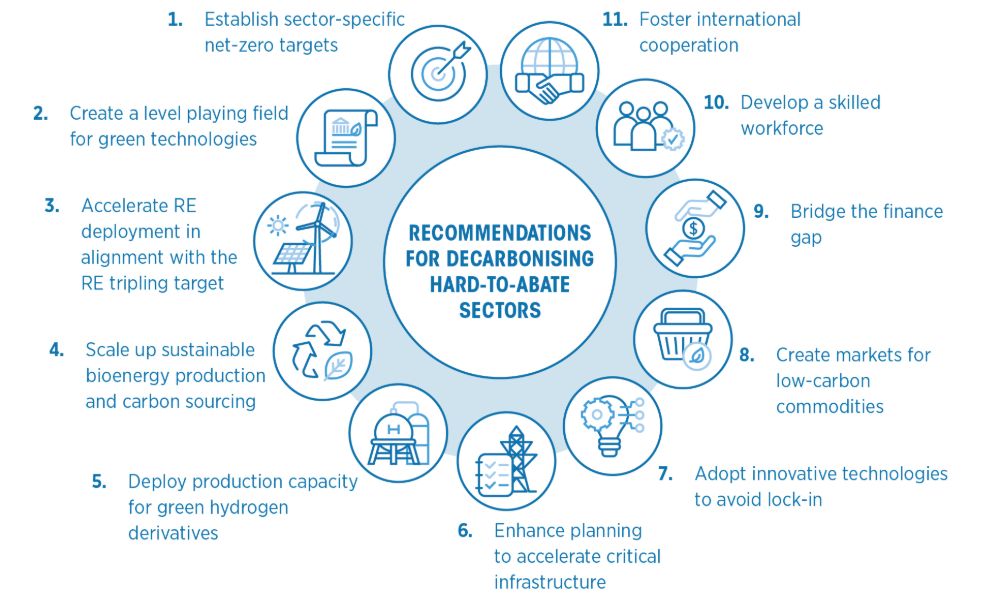

This report provides the following recommendations for governments:

On creating an enabling policy environment

1. Establish sector-specific decarbonisation targets. Governments can support the transition by establishing long-term, sector-specific, national objectives with clear intermediate milestones. Beyond national policies, countries can work with other countries towards further international convergence in the decarbonisation objectives for key traded commodities, such as steel, ammonia and methanol, as well as aviation and shipping fuels. These actions are particularly important for the international shipping and aviation sectors.

2. Take further steps towards creating a level playing field for green technologies. Governments can accelerate the adoption of green technologies in hard-to-abate sectors by implementing national carbon pricing policies that internalise the full value of the negative environmental externalities of fossil energy. Aligning energy taxes with decarbonisation objectives – for example, by reducing the relative taxation of electricity compared with fossil fuels – can also play an important role by driving the electrification of heat and transport applications. Furthermore, countries can work with other countries towards further convergence in international carbon pricing, for example through sector-specific international agreements.

On fast-tracking infrastructure deployment and technology adoption

3. Accelerate the deployment of renewable power supply. Governments can support the transition in hard-to-abate sectors by scaling up the deployment of renewable power supply in line with the COP28 pledge of tripling renewable capacity by 2030. This will require additional efforts, including a substantial scaling up of investments and updating of policies and regulations. Examples of the latter include streamlining permitting procedures and adaptations in power market design.

4. Scale up sustainable bioenergy production and sustainable carbon sourcing. Governments can support the transition in hard-to-abate sectors by working together to scale up global sustainable biomass supply chains. This can be achieved with policies that provide incentives for the production and/or use of bioenergy, coupled with strict sustainability governance procedures and regulations.

5. Kick-start deployment of production capacity for green hydrogen derivatives. Governments can accelerate the transition in hard-to-abate sectors by supporting the first wave of commercial-scale plants to produce low-carbon commodities – such as ammonia, methanol and iron – using green hydrogen.

6. Enhance planning to accelerate the deployment of critical infrastructure. Governments can support the transition in hard-to-abate sectors by strengthening cross-sectoral planning and international co ordination in energy, industry, trade, transport and the environment. They can also support the transition by accelerating the permitting and deployment of critical energy infrastructure including power grids (paired with smart electrification strategies), bioenergy conversion plants, hydrogen networks, and low-emission fuel terminals in ports and airports.

7. Drive the adoption of innovative technologies to avoid lock-in. Governments can accelerate the global transition in hard-to-abate sectors by prioritising and promoting the deployment of technologies that are consistent with net-zero emissions. Countries can also work together towards the widespread adoption of such new solutions, particularly in developing countries. This can be done through technology co operation programmes, the exchange of best practices, and many other methods to avoid lock-in of traditional technologies. 1

On driving markets and financial flows

8. Create initial markets for low-carbon commodities. Governments can support the transition in hard-to-abate sectors by establishing green public procurement programmes or mandates for low-carbon commodities. Countries can also work together to accelerate international convergence in definitions, standards, thresholds and certification procedures to enable the international trade of these low-carbon commodities.

9. Bridge the finance gap. Governments can drive an increase in global investment flows towards hard-to-abate sectors by working with the private sector and financial institutions to de-risk projects. Government support for project bankability can be implemented through several mechanisms, such as the provision of guarantees, concessional loans and blended finance.

On developing a skilled workforce

10. Support the development of a skilled workforce. Governments can play a significant role in developing the skills needed for the transition in hard-to-abate sectors. Potential measures include exchanging information on innovative technologies and best practices and providing financial support to specialised educational programmes and training.

On leveraging international co-operation

11. Foster international co-operation. Governments can work together towards mutually beneficial partnerships to decarbonise supply chains for industrial commodities. This can be done through co operative long-term investment planning that results in a lower cost of decarbonisation for all.

Figure ES3: Recommendations to support the transition in hard-to-abate sectors