Accelerating the transformation

3.1 Key considerations in the decarbonisation of hard-to-abate sectors

The technologies to decarbonise hard-to-abate sectors have seen significant progress in recent years and are, today, largely available. Innovation is one of the key means of further accelerating progress in deployable solutions in the hard-to-abate sectors.

In the transport sector, solutions exist to decarbonise the bulk of heavy-duty trucks, shipping and aviation. Battery producers have improved performance and reduced costs to a point that makes electric trucks technologically feasible even for demanding long-haul applications. Biofuels are a mature technological solution that can be scaled up to meet a substantial part of the needs of aviation and shipping. As the road sector transitions at an accelerated pace towards battery EVs, biomass feedstock currently dedicated to producing biofuels for cars and trucks will become available to produce SAF and shipping fuels.

The industrial sector has also seen substantial progress in recent years. Hydrogen-based DRI production has been proven at pre-commercial scale, and the first commercial-scale plants are being built or are at the advanced project stage, with a substantial pipeline of low-carbon steel production – around 80 Mt per year by 2030 – so far announced (LeadIT, 2024a). E-crackers, an electric alternative to the traditional steam cracker process in the production of HVCs, are being tested at a pre-commercial scale.

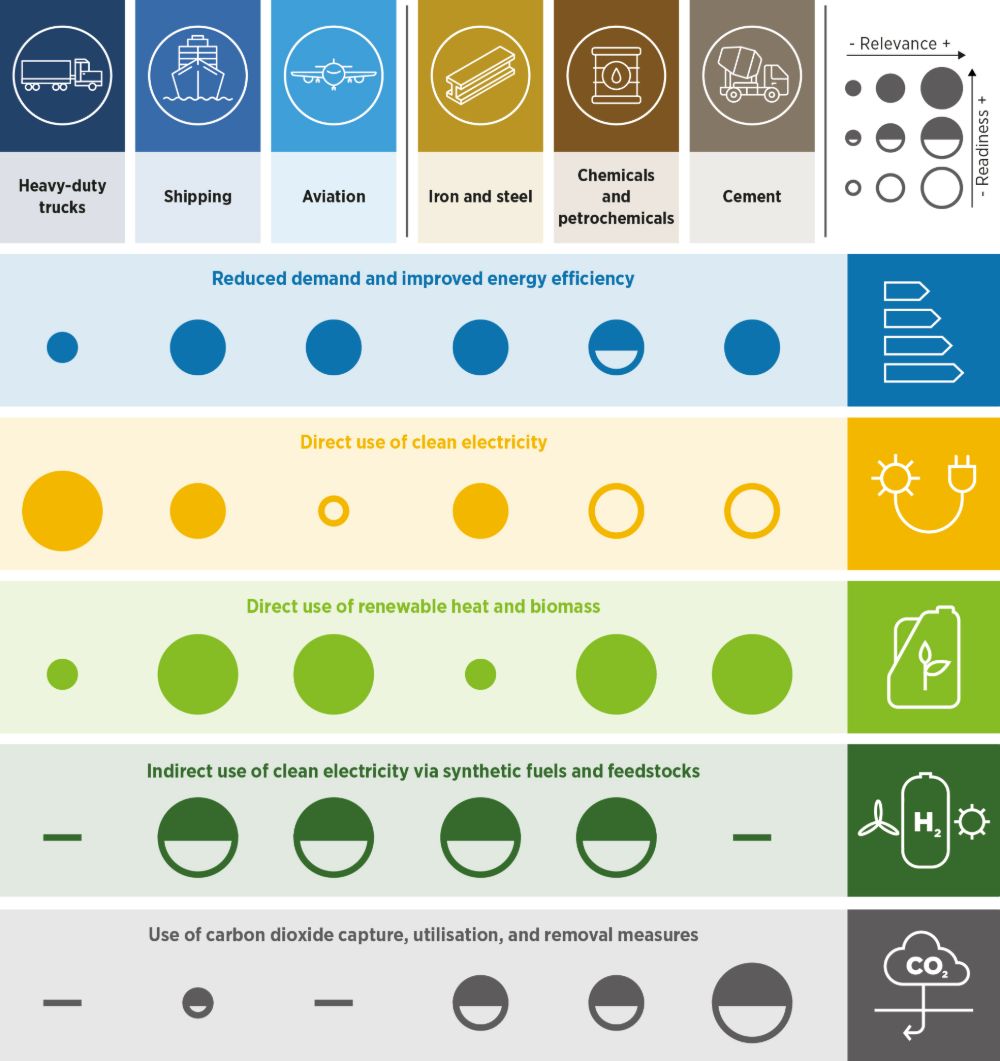

Renewables can play a central role in the decarbonisation of all hard-to-abate sectors. The drastic cost reductions observed in recent years make renewable power the cheapest source of carbon neutral energy worldwide. There is potential for further cost reductions through technological learning and economies of scale. Hard-to-abate sectors can be decarbonised with renewables using several solutions, including direct electrification, the use of bio-based fuels and feedstocks, and “indirect electrification” (i.e. the production of synthetic fuels using renewable energy and sustainable carbon sources).

Direct electrification will play an increasing role, with important contributions in multiple applications. Some of these solutions are already mature or are close to technological maturity. These include the use of electric arc furnaces for steelmaking, which will become more important as the share of recycled steel increases in the coming decades; battery electric trucks, which are at a technological inflection point and becoming increasingly available; heat pumps for low- to medium-temperature heating in industry; and cold ironing at ports. Some other applications of direct electrification, while having great potential, still need further development. These include electric crackers to produce primary chemicals; electrolysis of iron ores; and electric or hybrid aircraft and ships for short distances.

Figure 22: Summary of key technological pathways for decarbonisation and their readiness in hard-to-abate sectors

Bioenergy and synthetic fuels will play a critical, complementary role to electrification. Scaling up sustainable, low-carbon bioenergy solutions is not only key to the decarbonisation of shipping and aviation; it is also critical to the provision of feedstocks for chemicals and as a potential carbon source for synthetic fuels. Indirect electrification – via the production of renewable hydrogen – is also set to play an important role in achieving deep emission reductions in these sectors. Renewable hydrogen can do this as a reductant in the production of iron in primary steel production, as a form of synthetic fuel for shipping and aviation, and as a feedstock for chemical industries.

These pathways will have to be complemented by continual energy efficiency improvements, the application of the principles of the circular economy, and behavioural and process changes that reduce demand. Emissions can be further reduced through the application of CO2 capture, utilisation and/or removal measures, provided that these technologies achieve the necessary improvements in performance and economics to make them technically scalable and economically viable.

Although the technology associated with these pathways is increasingly available, in the absence of sufficiently high and widespread carbon pricing, a timely transition to renewables in hard-to-abate sectors will almost certainly require paying a premium over the cost of fossil-based systems. Cost differentials differ widely by sector and application. Battery electric trucks, for example, have a feasible pathway to reach cost parity and even become cheaper to operate than fossil counterparts in the short to medium term. The adoption of biofuels for shipping and aviation and bio-feedstocks for chemical commodity production will likely continue to come at moderate cost premiums. Synthetic fuels and feedstocks will likely result in relatively high premiums for the foreseeable future, although such cost premiums could be partially reduced by technology improvements.

Unprecedented social and political momentum, together with the increasing competitiveness of renewables and other enabling technologies, has resulted in increased action towards the decarbonisation of hard-to-abate sectors.

In the public sector, initiatives like the Breakthrough Agenda, Mission Innovation and the recently created Climate Club aim to catalyse transformative actions towards a low-carbon future in some hard-to-abate sectors. Along with these efforts, significant policies are setting ambitious targets and offering incentives to drive decarbonisation across industry and transport. These policies include the Inflation Reduction Act in the United States and the Clean Industrial Deal, the Net-Zero Industry Act, and the Fit for 55 package – which includes ReFuelEU Aviation and FuelEU Maritime – in the EU.

Collaborative ventures between the public and private sectors are fostering synergies to address emission reduction challenges holistically across sectors. These ventures include the Alliance for Industry Decarbonization, chaired by IRENA; the Industrial Deep Decarbonisation Initiative, led by the United Nations Industrial Development Organization and Clean Energy Ministerial; and the Decarbonising Transport initiative of the International Transport Forum. There are also several private sector-led initiatives, such as the Mission Possible Partnership, which addresses several hard-to-abate sectors, and the Getting to Zero Coalition, which has a focus on shipping.

But despite promising progress and increased attention from policy makers, none of the hard-to-abate sectors is on a trajectory compatible with reaching net-zero emissions by mid-century. The production volumes of green industrial commodities – such as primary steel and key chemicals like ammonia, methanol and olefins – are still negligible. Similarly, sustainable fuels for aviation and shipping represent a negligible fraction of these sectors’ total fuel consumption. Battery truck sales, though growing, represent a negligible fraction in terms of global road freight services.