Power market design

Overview

The power sector lies at the heart of the global energy transition, which relies on increased electrification of end uses and the adoption of variable renewable energy (VRE) sources, such as wind and solar PV, as the main source of electricity; however, today’s power systems embody an era in which generation depended on large, centralised and dispatchable power plants. It is therefore essential that power system structures evolve to meet the requirements of the renewable era.

IRENA’s work aims to inform discussions on power system organisational structures and how they can facilitate and accelerate the energy transition. It explores enablers of and barriers to the transition, including misalignments both within and beyond power systems, as well as the role of competition and its balance with regulatory and collaborative components.

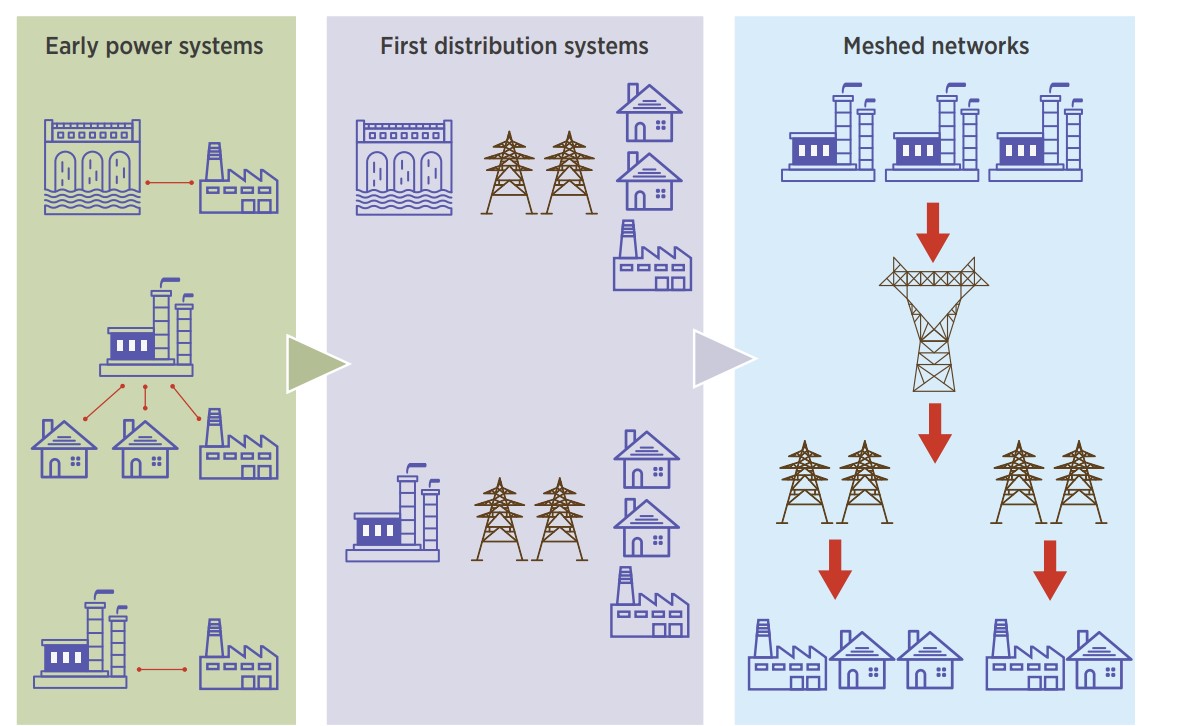

When power systems were first developed, electricity was produced close to the point of demand, which was typically an industrial load. As cities were electrified, distribution grids and later transmission grids connected urban centres with relatively distant power generators. Gradually, meshed networks were developed with multiple generators providing electricity to various loads, leading to the first national grids. As physical power systems evolved, the way that electricity was procured and allocated changed. Whereas at the outset bilateral agreements between the producer and the user were the norm, the advent of grids connecting multiple generators with multiple users made more complex organisational structures necessary to support the power system.

Power system organisational structures are designed around social and political goals and count on economic and physical allocation and procurement mechanisms to reach those goals, within the system’s technical limits. The way in which energy and flexibility services are rewarded brings crucial information in both the short term (“Should we provide this service now?”) and the long term (“Should we invest in the system and commission a new unit?”). Organisational structures convey the signals that determine the future of the power system

A new model for new challenges

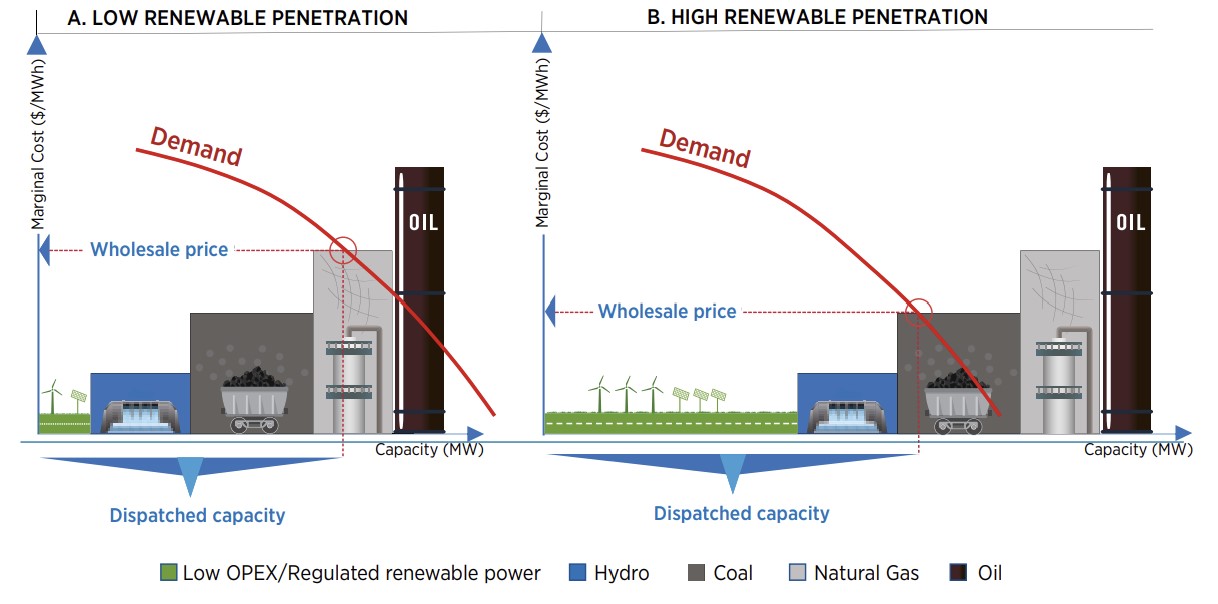

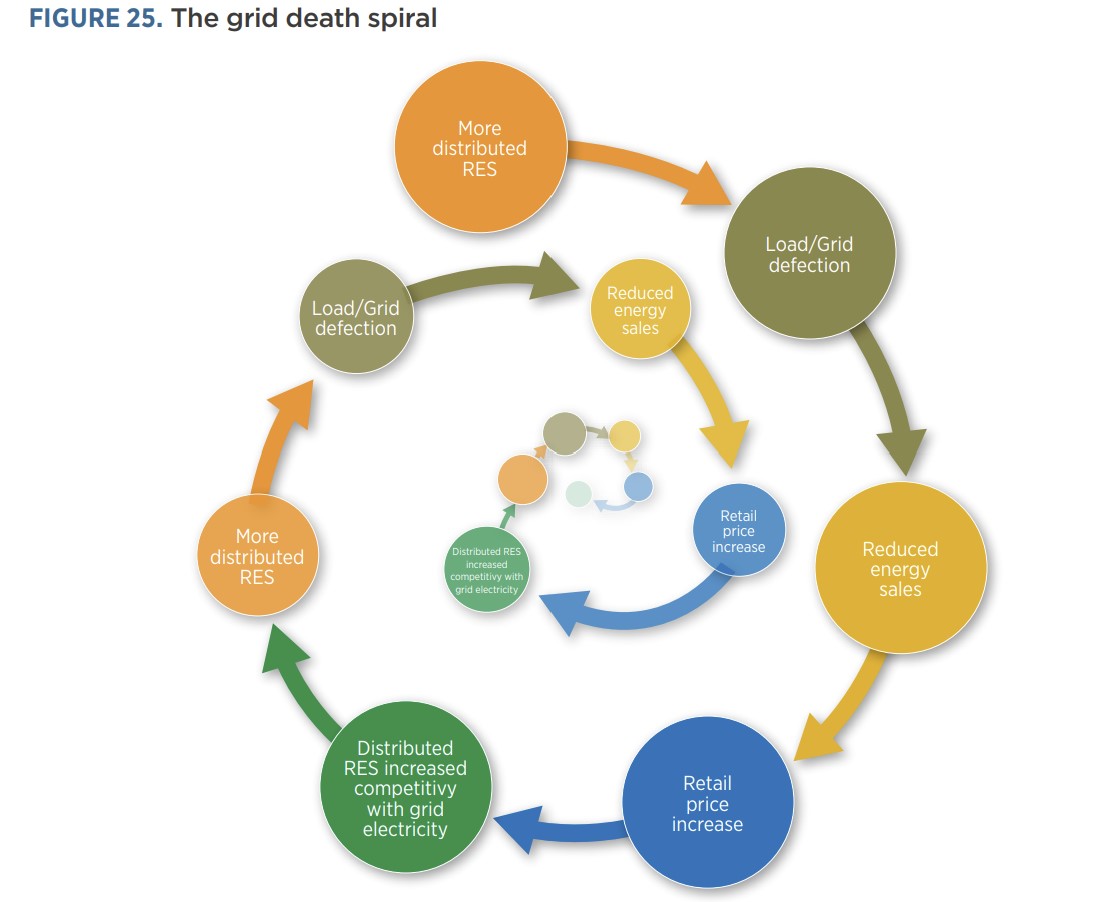

Power system organisational structures were designed with the blueprint of the fossil fuel era and had to be suited to both the prevalent technologies of a centralised energy system and the goals of the time. Governments now face a new challenge for the power sector: to successfully integrate renewable energy power plants at a rapid pace while maintaining acceptable overall system costs and fostering the maximisation of both system and social value – in a context of widespread electrification of the economy. Most energy transition policies put in place have not deeply considered their interaction with prevalent power system organisational structures. In most cases, they were designed to bypass the existing power system structures in order to facilitate the deployment of renewable energy. As the transition progresses, misalignments between power system organisational structures, support mechanisms and the techno-economic characteristics of renewables become more apparent. Some of them have become more common knowledge, with names like the “missing money problem” and the “grid death spiral”

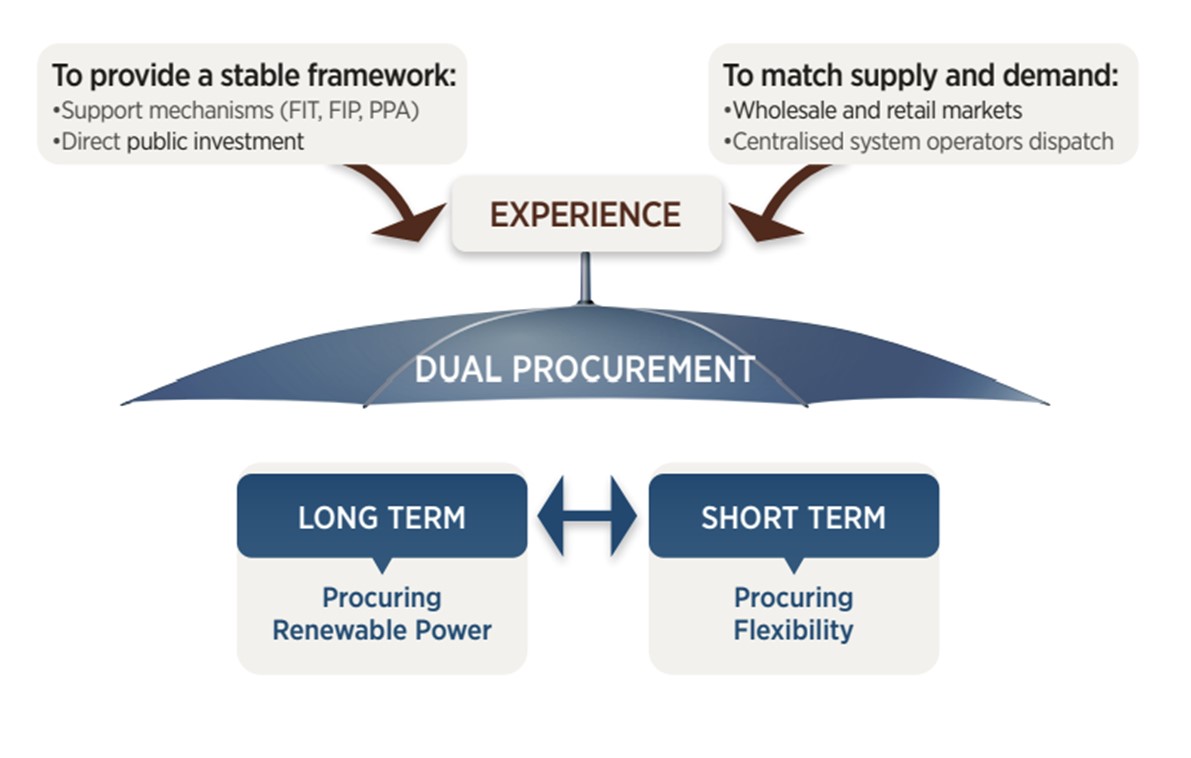

The dual procurement approach

Both regulated and liberalised power systems share the challenge of reformulating their procurement and allocation mechanisms to facilitate the transition process and to support the post-transition power system. This requires a holistic vision that captures the wider social and system value of electricity, while supporting the deployment of VRE and distributed energy resources, rewarding flexibility and system integration, and overcoming misalignments and constraints. In pursuing this goal, both regulated and liberalised systems need to find the appropriate balance between regulation, competition and collaboration to shape their procurement and allocation mechanisms.

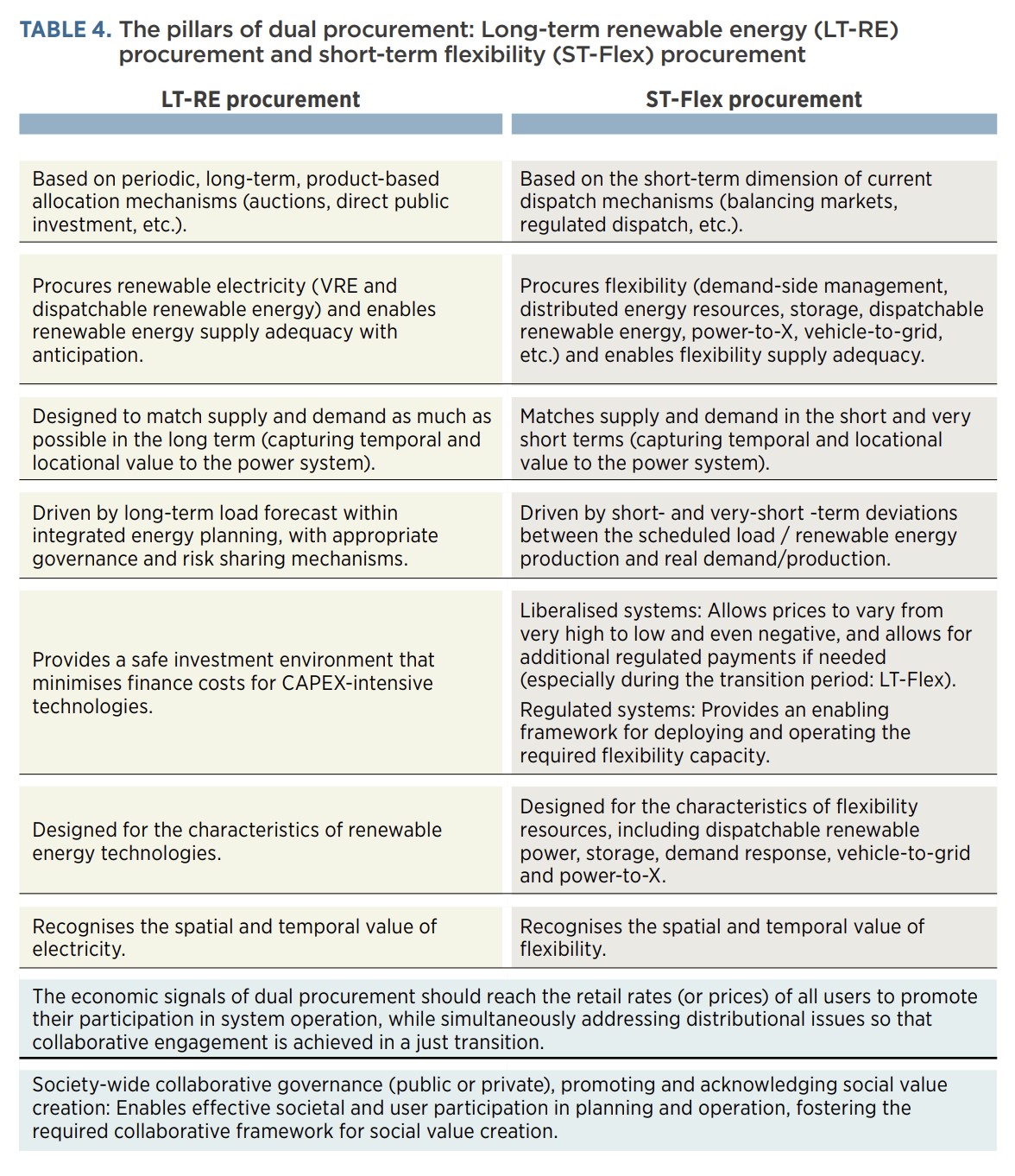

In the renewable energy era, power systems will have two fundamental but differentiated attributes: renewable-based generation (mostly VRE) and flexibility. Renewable electricity generators and flexible resources have different characteristics. Short-term marginal prices may become unable to guarantee cost recovery either to VRE plants as their increasing penetration depresses wholesale prices, or to flexible resources that are likely to be needed only occasionally.

Stable long-term payments are far more appropriate for procuring renewable generation, given their CAPEX-intensive nature.

Flexible resources are more likely to be efficiently procured through a short-term marginal pricing mechanism.

For these reasons (and many others, presented in our reports) IRENA proposes dual procurement.

The dual procurement proposal addresses this dilemma by splitting the procurement of renewable electricity and flexibility into two complementary procurement mechanisms that acknowledge the different characteristics of these services

The good news is that the dual procurement organisational structure does not need to be invented from scratch, because most of the tools and experience gained in the past can contribute to dual procurement. It could be argued that this proposal would be the natural evolution of current power systems if a holistic vision and associated policies were in place. In liberalised systems, auctions are already becoming one of the more common procedures to procure utility-scale VRE energy, with decreasing prices and increasing design complexity. Meanwhile, the day-ahead, real-time and ancillary services markets are evolving to the new normal of high VRE penetration, with incremental advances to properly reward and stimulate flexibility. In regulated systems, the long-term procurement of renewable energy generation is also advancing, through independent power producer auctions or targeted public investment programmes, while flexibility procurement and operation are evolving through integrated energy planning and public investment.

In countries with high shares of VRE and liberalised organisational structures, it is already possible today to perceive the “split” between the procurement mechanisms, with a sizable amount of electricity production coming from long-term energy contracts in the form of feed-in tariffs, feed-in premiums or bilateral/auctioned power purchase agreements. Indeed, the diffusion of auctions is creating a converging trend between liberalised and regulated organisational systems, with centralised power systems introducing a competitive scheme to procure renewable energy, and liberalised power systems reintroducing elements of state-driven energy policy.